18. The intro sheet is crucial as it includes the project name, a short description of the model’s intent/purpose, author details, and any applicable disclaimers, as shown in

Figure 2: Intro worksheet from the CAA's H7 PCM

19. More extensive guidance can also be provided if the model if of sufficient size andcomplexity to warrant this as well (see Figure 3).

Figure 3: Guidance worksheet from the CAA's H7 PCM

Inputs and Assumptions

Dynamic inputs vary over time, for example month-to-month or year-to-year.

Static inputs are those that do not change over time.

Figure 4: Input sheet from URNI's PC21 financial model

Figure 5: Capital base roll forward sheet.

Outputs

Figure 6: Outputs sheet from Ofgem's GT2 Price Control Financial Model PCFM.

Figure 7: Scenario analysis from the CAA's H7 PCM

31. Equally important to structure, formatting helps a user better understand how the underlying model inputs are derived as well as navigate quicker through the model.

32. Colour rules are a useful way to make model inputs understandable.

33. These can be used either on cell text or on the cell itself, and on the individual worksheets/tabs.

34. Text colours can distinguish between the types of inputs being viewed, to differentiate between:

• Inputs, or any hard-coded data, such as historical values or assumptions

• Formulas, calculations, or references from the same worksheet

• Formulas, calculations, and references to other sheets

• Links, inputs, formulas, references, or calculations to other Excel files

35. In the example below, from Ofgem’s RIIO-2 ET2 Price Control Financial Model (PCFM), we can see how this is used in practice on the cover page, Figure 8, and in the model itself, Figure 9.

Figure 8: Cover page of Ofgem's RIIO-2 Electricity Transmission PCFM outlining the key for text colour.

Figure 9: Use of text colour in Ofgem's RIIO-2 Electricity Transmission PCFM

36. Using cells colours to differentiate the input types is also effective, and a commonfeature of best practice financial models.

37. Below is an example from Ofgem's ED1 PCFM, where the Cover page sets out the keyfor cell colours (Figure 10) and uses this effectively within the model (Figure 11).

Figure 10: Cover page of Ofgem's ED1 PCFM outlining the key for cell colour

Figure 11: Use of cell colour with Ofgem's ED1 PCFM

38. Tab colours is another way to differentiate the functions that each part of the model undertakes.

39. Below is an example from Ofwat's PR19 Revenue Forecasting Incentive model, where the Cover page sets out the key for tab colours, Figure 10, and uses this effectively within the model, Figure 11. (ofwat.gov.uk)

Figure 12: Cover page of Ofwat's PR19 Revenue Forecasting Incentive model

40. General rules to follow when constructing, testing, and auditing financial models are included in the subsections below

41. General rules to follow when constructing, testing, and auditing financial models areincluded in the subsections below.

42. General rules to follow when constructing, testing, and auditing financial models areincluded in the subsections below.

Figure 14: Model map from the CAA's H7 Price Control Model

Delve into stock market predictability with Tobin's Q and dividend yield, challenging conventional views.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

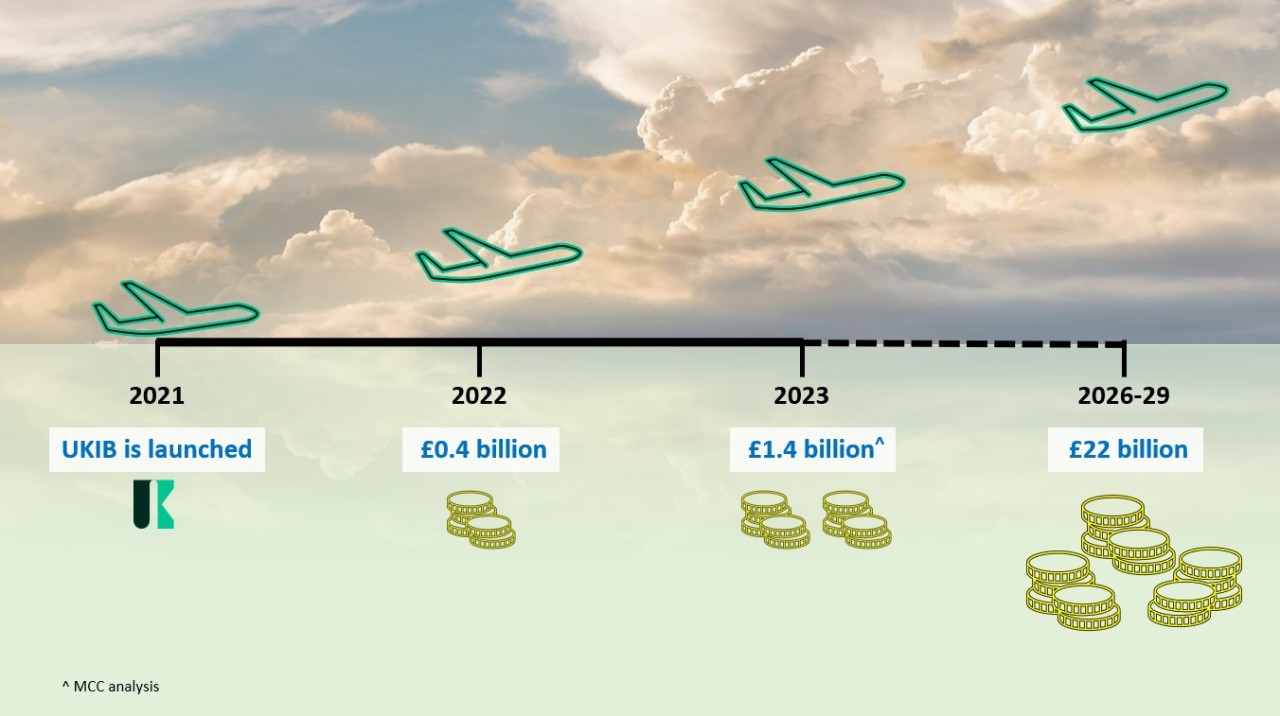

Explore how the UK Infrastructure Bank is shaping the UK’s green and economic transformation. This article reviews UKIB’s mandate, funding capacity, early investments, and risks, and assesses its potential to drive long-term, sustainable infrastructure growth.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

I was delighted that MCC's work was completed on time, and within budget, helping us deliver important changes and improvements, to the benefit of our stakeholders. MCC's report is published on the CCC website.

I am delighted to recommend MCC Economics. Specifically, I worked closely with PJ, who helped us with our Nuclear and CCUS projects. PJ helped us develop new policies and answer questions from our stakeholders. His support helped us deliver important changes and improvements, to the benefit of our stakeholders.

MCC Economics has helped us better understand the most important issues for our stakeholders, including: charges, shareholder returns, debt payments and inflation impacts.

I am delighted to recommend PJ and his team at MCC Economics. We've been working together on National Policy Statements to help meet net zero targets for 2030 and 2050. We initially appointed MCC Economics to support us on offshore wind consultation analysis and have recently reappointed MCC Economics to undertake a larger consultation analysis role across all sectors, including hydrogen, CCUS and networks. I can confirm that PJ and his team have shown excellent spreadsheet skills, alongside very good project management, planning and analysis skills, helping us deliver important changes, and continuous improvements, to the benefit of our stakeholders.

I am delighted to recommend PJ and his team from MCC Economics. They helped us with our price controls for Heathrow airport and for NATS (En Route) plc (the air traffic services provider). Specifically, the MCC team helped us deliver important changes and improvements to our financial models and supporting policy documents, to the benefit of our stakeholders.

I am delighted to confirm that I worked with PJ on a retail project in 2015. The project helped stakeholders understand electricity costs and charges. Specifically, the project helped us explain to stakeholders, internally and externally, why electricity charges differed across the regions (GB, NI & Ireland). PJ was a key member on the project team, which helped deliver changes and improvements in the understanding of energy retail.

.png)

Evidence-based analysis for transparent, defensible, and effective decision-making.

© All rights reserved – MCC Economics 2026.