MCC Economics publishes independent analysis and commentary on issues at the intersection of economics, finance, and regulation. Our publications draw on experience from projects across energy, water, infrastructure, and public policy - providing evidence-based insights that support transparent, accountable, and effective decision-making.

.png)

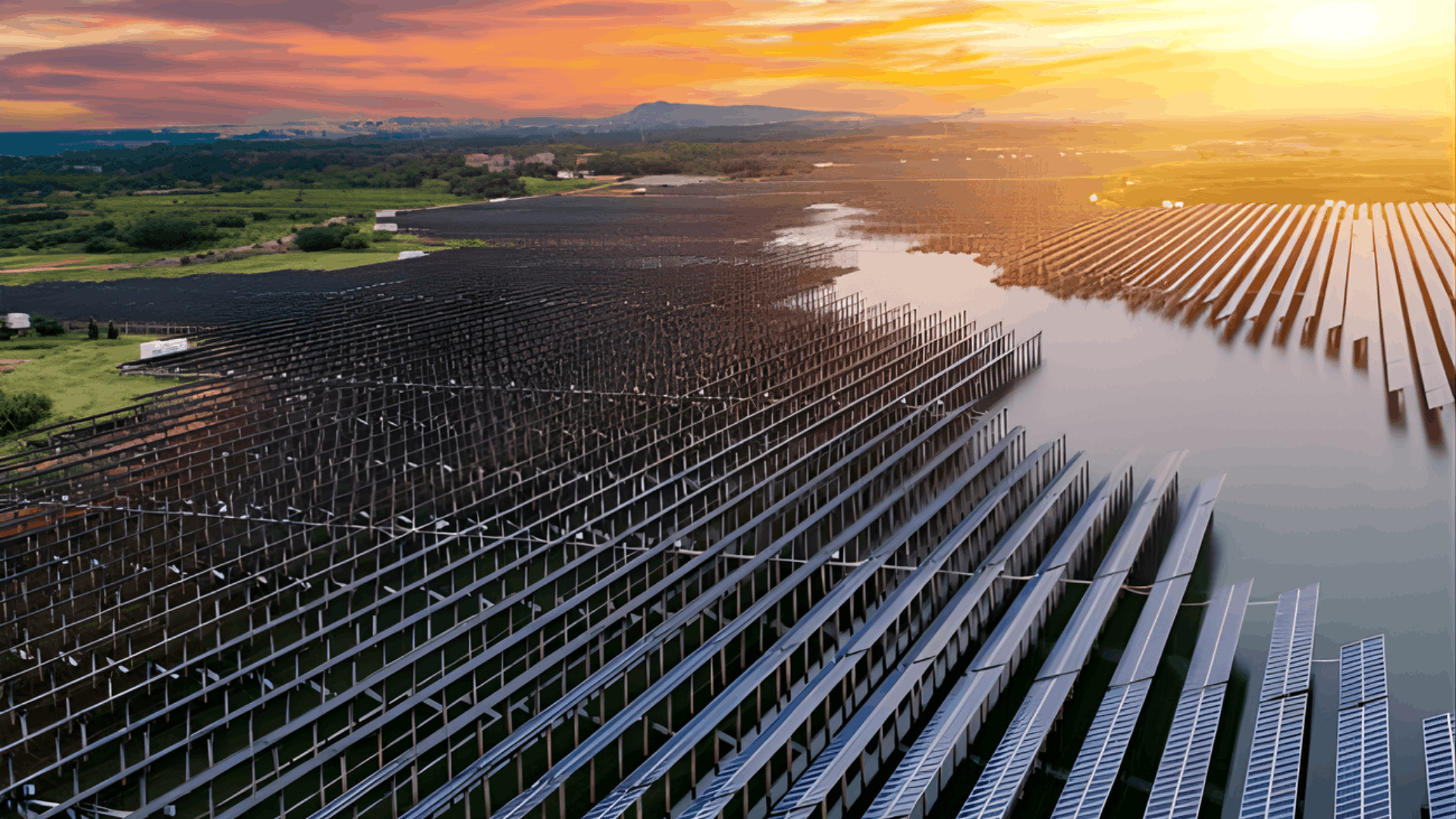

Explore our latest paper which examines Abu Dhabi’s solar approach—centralised utility-scale vs. distributed rooftop generation. Finds rooftop PV still uneconomical for heavily subsidised user groups but cost-effective for industry and commerce, suggesting subsidy reforms to unlock distributed solar for 2050 climate goals.

Abu Dhabi faces a strategic choice in scaling up solar energy: centralised mega-projects or decentralsed rooftop systems. This paper by our Director PJ McCloskey and analyst Rodrigo Remor analyses why distributed solar uptake remains low in Abu Dhabi and evaluates its economic viability under current conditions. Abu Dhabi has so far favored large solar parks (e.g. the 1.17 GW Noor Abu Dhabi plant) while rooftop solar adoption is minimal (~2.94 MW on government buildings by 2020, <1% of Noor’s capacity). Given the UAE’s net-zero commitment and Energy Strategy 2050 targets (44% renewable electricity by 2050), the study explores whether decentralised solar could play a larger role and what policy shifts might be required.

This paper evaluates the economic viability of decentralised solar systems in Abu Dhabi. By analysing levelised cost of electricity (LCOE), net present value (NPV), and internal rate of return (IRR) across customer groups, it finds that while rooftop solar generation is not yet cost-effective for heavily subsidised sectors, it remains viable for industrial and commercial users. The study suggests that subsidy reform could significantly improve the financial appeal of decentralised systems, aligning with Abu Dhabi’s decarbonisation targets under the UAE Energy Strategy 2050.

About

Abstract

Explore our latest paper which examines Abu Dhabi’s solar approach - centralised utility-scale vs. distributed rooftop generation. Finds rooftop PV still uneconomical for heavily subsidised user groups but cost-effective for industry and commerce, suggesting subsidy reforms to unlock distributed solar for 2050 climate goals.

.png)

Evidence-based analysis for transparent, defensible, and effective decision-making.

© All rights reserved – MCC Economics 2026.

.png)

%20(1).png)

.jpg)

.png)

-min.jpeg)

.jpeg)

.png)

.png)

.png)

.png)

.png)