1. MCC Economics (we or MCC) were commissioned by the Consumer Council for Water (CCW) to review Ofwat’s final determination for the weighted average cost of capital (WACC) allowance as published in December 2024 at the end of Price Review 2024 (PR24).¹

2. Ofwat has run a robust and lengthy PR24 process. Customers have contributed more than ever before. However, Ofwat introduced some late and material changes which may have unintended adverse consequences for customers, including: 1) the October 2024 consultation on incentives (the ‘outturn adjustment mechanism’); and 2) deciding to aim up when choosing a cost of equity allowance in contrast with its ‘final methodology’.

3. There appears to be an upward tendency in the ranges chosen for the major sub-components of the WACC, mostly driven by financial conditions faced by specific companies that have moved away from the notional capital structure, adopting highly geared structures and weakening their financial resilience. These conditions have arisen not from external market pressures but from choices made by their shareholders. Including those costs in the final determination risks shifting the consequences of those decisions onto customers.

4. Ofwat has previously been clear that companies are free to deviate from the notional structure, but that they do so at their own risk. However, this principle may not have been consistently followed in the final PR24 decision. The result is a WACC that may overstate the returns needed to attract finance for a well-run, notionally structured company.

5.Accordingly, we ask:

- Has Ofwat’s decision to adopt upper-bound values for some WACC components resulted in a shift of risk from shareholders to customers? If so, what was the size of this shift?

- Do the allowances reflect the lower investor risk created by the package of protections introduced in PR24?

6. Has enough been done to prevent moral hazard, so that the costs of inefficient financial strategies are not borne by customers?

7. Using MCC’s alternative values for the main components of WACC, which are based on market evidence and notional efficiency assumptions, we calculate that the allowance could have been set 1.08% lower. That difference, if applied across the sector’s Regulatory Capital Value (RCV), could save customers around £5.4 billion over the next five years - the equivalent to about £41 per household per year.

8. This is not a criticism of Ofwat’s overall framework. Our report offers a different view on how its own principles and evidence could have supported a lower WACC, and thus a more balanced outcome for customers.

9. Notably, the companies now seeking a redetermination from the Competition and Markets Authority (CMA) are amongst those with the most highly geared structures and the largest departures from the notional gearing assumption of 55%.

10. Fortunately, the CMA has an excellent opportunity to protect water customers and the water industry from any moral hazard.

11. Accordingly, we ask if the CMA could:

a) set a lower WACC allowance to reflect the available evidence;

b) allocate risks to companies rather than customers;

c) consider whether the ‘growth duty’ is consistent with aiming up;

d) consider the moral hazard risk - where highly geared companies receive a higher WACC allowance - and the related ‘resilience duty’;

e) consider whether a higher WACC allowance will lead to higher water investments or higher dividend distributions given the totex incentive mechanism is a much stronger incentive not to invest.

12. Ofwat has faced a challenging task in PR24, amidst heightened concern about the performance and conduct of the water companies, and the clear need for remedial action and additional enhancement investment on their part. The latter was a major theme in Ofwat’s decision and it has influenced Ofwat’s choices more than any other factor. We see it used as a justification for Ofwat’s choices at each major decision point in the determination. However, customers should not compensate shareholders for the consequences of their own inefficient practices and risky financial structures.

13. Ofwat is committed to this principle, but may not have given it practical effect in its decision making despite explicit warning (see 2004 for example). If Ofwat had done so, it could have chosen WACC components toward the centre of its ranges and its final values for debt and equity would be lower. Past guidance (2004 and 2024) explicitly stated Ofwat’s expectation that companies retain earnings to support large capital programmes.

14. While Ofwat introduces several mechanisms that reduce exposure to outlier outcomes, it is unclear whether these mitigations have been consistently reflected in the calibration of the WACC point estimate. Ofwat has implemented a material recalibration of the risk and return framework including enhanced true-ups and reduced performance targets. These adjustments give investors more stable (and probably higher) returns.

“...the PR24 draft determinations represent a material recalibrationof the incentive package which increases the levels of risk protection compared with our final methodology (and by extension, PR19)”.

15. If Ofwat had placed greater weight on certain market-led inputs or placed less emphasis on investment delivery incentives, a materially lower WACC could have been justified - potentially reducing bills by a significant amount. An illustration of what this reduction could look like is presented below.

16. The WACC allowance (%) is multiplied by the Regulatory Capital Value (RCV) to calculate the monetary (£) allowance, paid for by water customers each year. The RCV could be close to £100 billion by the year 2027-28 (the midpoint of the next price control). If so, each 1% on the WACC allowance will be worth £1 billion per year.

17. Replacing Ofwat’s final determination with the market-led values calculated by MCC would reduce the WACC allowance by 1.08%, as shown in Table 1. This would have reduced customer bills by £5.4 billion over 5 years2, which is worth £41 perhouse hold per year.3

18. The ‘market-led view’ is further supported by the following tables and the analysis presented in the remainder of this report

19. We now step through each component of the WACC to outline our assessment and the alternative conclusions we have reached.

20. Inflation assumptions are required in multiple parts of the WACC assessment. Wehighlight two areas: 1) the cost of debt, and 2) the TMR. In general, lower inflation assumption yield a higher WACC allowance.

21. Ofwat uses 2% for inflation expectations within the cost of debt. This 2% assumptionis lower than: 1) the Office for Budget Responsibility (OBR) who refer to 2.4%; 2) the Bank of England (BoE) gilts data which suggest approximately 3.%; and 3) the BoE survey response (see question 2c) dated February 2025 of 3.6%. The potentialdifference is shown below

Figure 1: Inflation expectation options for the cost of debt

22. Our assessment is that OBR’s estimate of 2.4%, which is arrived at by their forecast model, is the most appropriate for the calculation of the WACC components. This is due to it being theoretically and empirically sound, accounting for variables that are likely to affect long-term inflation, and not being influenced by short-term changes in market expectations.

23. Ofwat uses approximately 3.7% for outturn inflation from 1900 to 2023 within the Total Market Return. Ofwat’s assumption relies on a CPIH back cast. By contrast, other sources (the Office for National Statistics (ONS), the BoE and Dimson Marsh Staunton) do not use the CPIH back cast. The potential difference is shown below. Also, we suggest that the averaging technique for inflation estimates (arithmetic or geometric) is consistent with the averaging technique for TMR outturn values.

Figure 2: Inflation outturn options for TMR

24. We believe Ofwat’s approach to embedded debt should be reconsidered, as it seems to depart from the principle of assessing the notional efficient company. Ofwat does this in two places:

“Instead of calculating embedded debt costs over 2024-25 by reference to the level of RCV growth and notional gearing, our calculations are made on the basis of actual and forecast debt issuance as proposed by the water companies”

“The sample of debt instruments on which our calculation is based includes companies and debt instruments that carry a credit rating that is lower than that targeted for the purposes of the notional structure. Typically, a lower credit rating aligns with a higher interest rate. In some cases, companies have recently issued debt at interest rates well above those that might be expected for an efficient company operating with the notional capital structure.”

25. Ofwat goes on to note concern with its chosen approach, saying:

“Over time, this discrepancy could have a more significant impact on the benchmark used for setting the embedded cost of debt.”

26. While we think these issues should be rectified, their materiality is not clear from Ofwat’s analysis. Ofwat has included actual company data that may reflect inefficient costs, in order to better reflect prevailing market realities. This trade-off between realism and notional efficiency merits further scrutiny, as they tend to favour companies, especially those that chose to adopt riskier financial structures.

27. Potentially more consequential, there is a further concern with Ofwat’s approach. The relative debt costs for the water companies have spiked over the past 2 years and we believe Ofwat has not adequately explored the reasons for the spike. A more detailed exploration would likely have concluded that shareholders and companies are experiencing the consequences of their own inefficient practices and risky financial structures. As such, customers should not bear the burden of the relative spike in debt costs.

28. The recent spike in debt costs is clear in Figure 3. There has been a material change in relativity between the water sector and the broader index. Companies with the highest financial distress or highest gearing (Thames, Southern, Anglian) are way above benchmarks and the entire sector has lost its debt cost advantage relative to benchmarks.

29. Ofwat ought to have drawn from its Monitoring Financial Resilience Reports. For example, in 2022-23 it observed that:

“Current macro-economic conditions highlight the importance of companies maintaining headroom and financial flexibility to manage periods of volatility… higher than expected inflation and rising interest rates have also placed upward pressure on operating, capital investment and financing costs. This has caused short-term cash pressures for some companies that has impacted on financial ratios and credit metrics”

30. Ofwat now rates 10 of 16 companies at “action required” or “elevated concern ” for financial resilience. In Figure 4, we illustrate that concerns about financial resilience are strongly related to gearing levels above the notional benchmark.

Figure 4: Gearing and Ofwat resilience rating (red box: action required; yellow box: elevated concern)

31. With high gearing driving concerns about financial resilience and debt costs, Ofwat ought to have placed greater weight on benchmarks (e.g. the iBoxx A index). This would have been consistent with setting a cost of debt for the notional efficient company. Instead, Ofwat diminished the role of the index by no longer using it as an upper bound. It justified its change of approach by referring to “current market dynamics”, although the specific rationale could benefit from further elaboration.

32. We think the index-led approach should dominate, instead of the balance sheet approach. At the very least it should set a maximum value of 4.59% nominal compared to Ofwat’s final value of 4.82% nominal.

33. Alternatively, in its 2022 final approach, Ofwat observed that the iBoxx index was 14bps below its 20-year benchmark estimate. Based on Figure 3, this appears to have been a consistent pattern for many years. If Ofwat had applied this long-termrelativity in its final decision, it would have generated a lower cost of debt.

Figure 5: Ofwat’s decision on the cost of embedded debt

34. Observed spikes in sector debt costs appear closely linked to financial distress and elevated gearing among a subset of companies, which reflects specific inefficient financial strategies, not market-wide inefficiencies.

35. While Ofwat’s choice to reflect actual debt issuance conditions may aim to ensure realism, doing so risks embedding the consequences of aggressive structuring decisions into the price control framework. This raises the question of whether allowances are being calibrated to reflect efficiency or to accommodate fragility.

36. Ofwat starts with the average of the A and BBB-rated iBoxx GBP non-financials 10+indices as its Benchmark Index. It then considers whether a benchmark adjustment should be employed to reflect the circumstances of the water companies. It applieda negative benchmark adjustment at PR19 and a zero adjustment at the PR24 draftdeterminations.

37. We agree with this broad approach, however, Ofwat’s implementation contains similar faults to its approach for embedded debt. Ofwat observes that “the cost of debt has increased above the benchmark index” but it then does not satisfactorily account for the drivers of that increase.

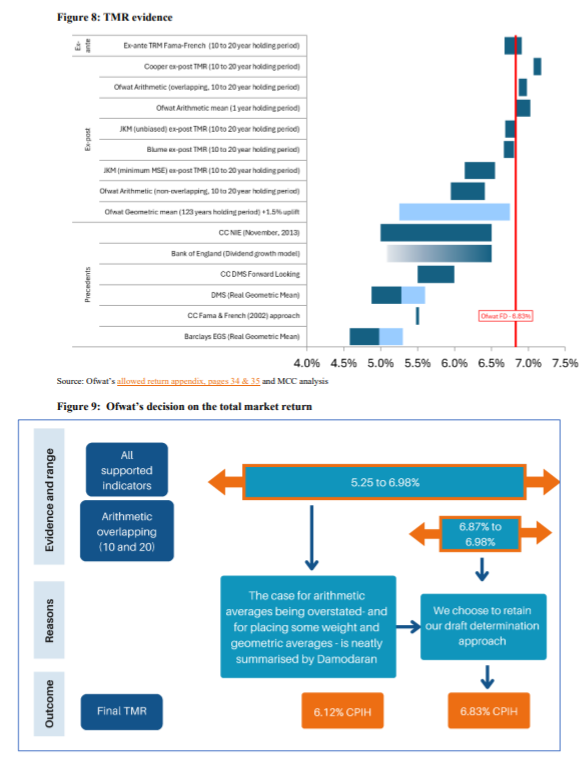

38. Ofwat correctly expresses concerns about employing the recent increase it has observed to set its benchmark adjustment:

“We note that the observations with the greatest spread to the benchmark are driven by companies with credit ratings that arebelow the notional benchmark.”

“For the six months to the end of September, our data cut off, the average increase for the four companies above our benchmark index was 24 bps. Since that date the difference has reduced”

“There is significant uncertainty as to whether the spreads to our benchmark index will persist.”

39.In addition, we offer the following observations.

40. We provide further detail in Table 6 below. The value of the benchmark adjustment is very important because it will endure for the entirety of the PR24 period. While the cost of new debt is subject to a true-up, the benchmark adjustment is not.

41. Ofwat justifies its choice of a 30bps benchmark adjustment by citing current evidence of elevated debt spreads and the large scale of funding needed to support investment programmes over the next 5 years.

42. We believe there may be scope for reconsidering how judgement has been exercised in this context. Ofwat ought to have placed more weight on the long-term trend. More importantly, it ought to have recognised that the current spike in debt costs have their foundation in the aggressive financial structures employed by shareholders which have made the companies less resilient to short-run cash flow disturbances. Additionally, Ofwat has selected a benchmark adjustment value of 30bps, higher than its own stated estimate of 24bps, which may merit further scrutiny.

43. We believe a benchmark adjustment of -15bps is more consistent with the long-term trend and the characteristics of the notional efficient company. This is the value Ofwat proposed to employ in its final methodology.

44. Ofwat considered the option of introducing a true-up for the benchmark adjustment but dismissed it “…because it would represent a late change to the PR24 methodology and would be accompanied by implementation challenges”. We note that Ofwat has introduced numerous late changes to its PR24 methodology in its final decision, especially in terms of the risk balance in its decision. Given the importance of the benchmark adjustment and the uncertainty about its stability we believe Ofwat ought to have pursued this option.

Figure 6: Ofwat’s decision on the benchmark adjustment for the cost of new debt

45.Having assessed the cost of debt, we now turn to the cost of equity, the other key pillar of the WACC.

46. Ofwat correctly employs the CAPM as its primary tool for estimating the return on equity. Other models are advocated by some of the companies and there is some theoretical support for these models in the finance literature. However, these models are unstable and are rarely employed in practice. Using these models as a key element of the decision-making process would be a substantial departure from finance and regulatory best practice.

47. Ofwat employs a 10-20-year horizon in its CAPM in line with the UKRN’s 2022 methodology. There is a valid school of thought that the term of the CAPM should be aligned with the term of the regulatory determinations, that is, 5 years. This is on the basis that regulatory determinations effectively reset the future expected returns, as would be the case for a resetting bond. However, we recognise that this approach is rarely used and would be a departure from current practices in UK regulation. Therefore, we apply the 10-20-year horizon employed by Ofwat.

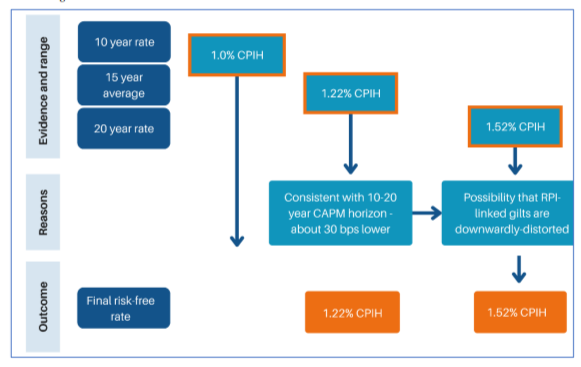

48. In PR19, Ofwat used the 15-year RPI-linked gilt rate as its proxy for the risk-free rate. In PR24, Ofwat now uses a 20-year proxy “against the possibility that RPI-linked gilts are downwardly distorted proxies for the true risk-free rate”. There are three issues with Ofwat’s choice of a 20-year proxy:

• First, it introduces an inconsistency with its 10-20-year CAPM horizon. There is a fundamental principle that the components within the CAPM should be applied consistently. For consistency within the CAPM, Ofwat should employ both 10- and 20-year estimates.

• Second, Ofwat diligently assesses all of the evidence suggesting that RPI-linked gilts are downwardly distorted and correctly finds the evidence is not convincing. For example, in respect of a potential convenience yield, Ofwat concludes “our position remains that there is insufficiently strong evidence to accurately calibrate an adjustment at our 10-20-year CAPM horizon”.

• Third, it is an idiosyncratic approach unique to the UK regulatory framework to look beyond gilts as a proxy for the risk-free rate. It departs from the well-established and near universal application elsewhere.

49. Ofwat’s justification of a “possibility” of downward distortion does not satisfy the principles of sound regulatory judgement. Ofwat should have concluded that the evidence best supports the continued use of 15-year gilts from its PR19 determination. If it had done so, Ofwat indicates its risk-free rate would have been “lower by c.30bps”.

Figure 7: Ofwat’s decision on the risk-free rate

50. Ofwat has consistently employed a total market return (TMR) framework for many years, in line with the UKRN’s 2022 methodology. During the period of low interest rates this approach yielded returns on equity well in excess of the risk-free rate. It is a natural consequence of the TMR approach that the gap between debt and equity should narrow when interest rates are higher.

51. The alternative approach is to employ a fixed MRP as is the case in Australian energy regulation. The fixed MRP approach recognises that debt and equity are alternative sources of capital, and their relative costs ought to move in step.

52. However, now is not the time for a change. Doing so may subject customers to windfall losses after supporting relatively high returns on equity. Such a change would also not be consistent with the principle of regulatory consistency and predictability.

53. Ofwat correctly identifies the range of indicators available to estimate the TMR, however, it has selected its range from only two of these indicators. We consider Ofwat has erred by excluding relevant indicators from its range.

• First, Ofwat correctly outlines the case for arithmetic averages being upwardly biased. If Ofwat had employed the geometric average, the bottom of its range would have been 5.25% rather than 6.87%.

• Second, Ofwat notes “we continue to consider the greater relevance of the 'investor' perspective would support continued weight on the horizon-weighted indicators, such as Blume and JKM estimators, which occupy a lower part of the overall range from 6.14% to 6.83%”. However, Ofwat has not taken the next step to incorporate these indicators when setting its range.

54. In Figure 8, we illustrate the full set of indicators available for forming a view on the TMR. Ofwat’s decision suggests heavy weighting towards ex-post and arithmetic averages.

55. However, we consider there is a strong case for using the geometric average plus an uplift to arrive at a TMR of 6%. A TMR of 6% or 6.5% can also be achieved by putting more weight on Blume, JKM, precedents and non-overlapping estimates.

56. We largely agree with the approach Ofwat has used to form its equity beta range.We believe Ofwat has appropriately considered and decided on estimation period,omitting certain periods, impact of the PR24 capital programme and comparators.However, Ofwat’s beta decision(s) look high as demonstrated below.5

57. Further, we think that Ofwat could have better accounted for the adjustments to its risk and return package. Ofwat correctly observes:

“our final determinations provide enhanced risk protection to company performance on costs and outcomes compared to PR19,in ways we would expect to reduce beta risk”

58. An appropriate approach would have been to choose a beta no higher than the mid point of the range, such as an unlevered beta of 0.25 or an equity beta of 0.55.

Figure 11: Ofwat’s decision on re-levered equity beta

59. It may be beneficial to also consider a different methodology for the estimation of beta, which accounts for the volatility in the variance of equity over time. The methodology currently employed by Ofwat, Ordinary Least Squares (OLS), assumes that the variance of equity values is constant, which might not always hold due to changes in market conditions. Considering these changes in variance, a model such as Generalized Autoregressive Conditional Heteroskedasticity (GARCH) could lead to more accurate estimates of beta. GARCH models are used in the financial sector to estimate time-varying volatility in time series data, and are employed by other regulators, such as Ofgem, in their price reviews. Despite the increased complexity compared to OLS, we believe this methodology is better suited for estimating betas in a regulatory context, due to it presenting more efficient estimates.

60. Our calculations for raw beta and unlevered beta, shown in Table 7, show that the GARCH methodology consistently leads to smaller values of beta than OLS. Depending on the sample period, the GARCH model leads to unlevered beta values even lower than the 0.25 mentioned above.

61. Ofwat settles on a range for the cost of equity of 4.58% to 5.07% with a mid-point of 4.825%. We have already outlined our views on why the components used in calculating this range lead to a distorted outcome.

62. Ofwat then chooses a point estimate above the top of its range at 5.10%, adopting an “aim up” adjustment to midpoint of 29bps. However, this decision follows a comprehensive set of risk-reducing measures introduced in PR24, including enhanced true-ups, reduced performance targets, and improved cost protections. These materially lower the volatility and downside risk for equity investors.

63. Ofwat offers two reasons for its choice in its allowed return appendix, page 84, though these may warrant further evaluation, particularly in light of alternative interpretations of the evidence.

64. The first reason given was that “investor sentiment towards the water sector is currently low”. We note that these sentiments are likely a reflection of aggressive financing structures and culture and leadership issues, as noted by Ofwat in 202, as well as possible large fines due to breaches of environmental permit conditions. However, these are company-specific, not sector-wide risks, and should not shift cost burdens onto consumers.

65. Second, “companies and their consultants have argued that a large capital programme increases risks associated with capital intensity”. Ofwat has considered this submission and correctly dismissed it, as this is a largely diversifiable risk and ought not to play a role within WACC allowances.

66. By contrast, Ofwat outlines a cogent case for choosing a value at the mid-point including in its allowed return appendix:

• consistency with UKRN’s 2022 Guidance

• increased level of risk protection

• falling interest rates

• additional indexation returns

• opportunities to outperform the investment programme

• record levels of equity raised (£4.6 billion) by the sector since 2021

• supported by Ofwat’s advisors

67. We agree with this latter reasoning and consider that the case is made for choosing at the mid-point of a fair range. Best practice application of the CAPM is to make the best estimate of the cost of equity consistent with the principles underlying each component. Where there is a specific requirement or asymmetric risk in play, best practice is to avoid adjustments within the CAPM. Instead, adjustments ought to be made elsewhere within the cashflows.

68. We recognise the data and models to support the CAPM are imperfect, and reasonable analysts may reach different conclusions. However, the cost of equity allowance appears to be set toward the upper end of the evidence range, which may merit reconsideration.

Figure 12: Ofwat’s decision on the cost of equity point estimate

69. Cross checks on the cost of equity are well known for their imprecision. If there was a highly credentialled top-down measure, it would be preferred to the model approach usually employed. We are therefore left with an imperfect set of indicators to help form an overall impression. We largely agree with the approach employed and conclusions reached by Ofwat in this area.

70. It is a natural consequence of the fixed TMR approach that the gap between debt and equity will narrow when interest rates are higher. When comparing debt and equity premia it is important to use measures of debt that are consistent with the notional benchmark.

71. Ofwat compares the debt premium against the mid-point of its cost of equity range, 4.82%. Ofwat concludes:

“We find the implied premium against our benchmark to lie in a range of 1.63%-2.38%. We were not persuaded that such a premium was clearly too low.”

72. In any case, the premium was up to 50% lower previously, for the ten-year period between 1995 and 2005, Asset Management Periods 2 and 3.

73. Despite the recent challenging circumstances facing the water sector, Ofwat sees no concern arising from MARs. Ofwat concludes:

“The September 2024 average MAR premium was 9%. This is closely aligned with the long-run average for the sector of 10%.”

Figure 13: Water sector MAR premia to RCV, listed water companies, Jan 1993 to Sep 2024

74. Accordingly, it is difficult to see how any negative investor sentiment is being reflected in the market values for lower geared listed water companies.

74. We agree with Ofwat that multi-factor models do not meet the necessary standard to be given weight in regulatory decision making.

75. Ofwat concludes that there is a “broadly symmetrical distribution of returns at package level”.

76. This is one aspect where we disagree with Ofwat. We believe that Ofwat has not fully reflected the changes which reduce risk for investors. Had it done so, it could have concluded there is a material prospect of the companies exceeding the regulatory return on equity.

77. Ofwat also considers potential asymmetry in its CAPM parameters. It correctly concludes that each component is more likely to be too high rather than too low.

79. The scale of the enhancement programme appears to have been a key factor in Ofwat’s decision to allow a higher WACC. It is referenced prominently in multiple places, for example:

“The increase against the allowed return set at PR19 mainly reflects an increase in the cost of finance. But it also reflects revisions to the weight we place on data we use to inform our decisions on the allowed return and our decision to apply an allowed return on equity towards the upper end of our stated range, in order to support the delivery of increased investment in the 2025-30 period.”

“... an allowed return on equity that is in the upper-end of our range should support companies to secure external financing required to deliver the PR24 investment programme over 2025-30.” (2024, allowed return appendix page 84)

“Overall, we conclude that a benchmark adjustment of 30bps to be reasonable, taking account of the current evidence of elevated debt spreads and also the need for water companies to raise significant finance to support their 2025-30 investment programmes.”

80. In isolation and at face-value, the proposed uplift in the size of the enhancement investment programme is striking: £44,489million (£2022-23) for PR24 compared to £8,278million (£2017-18) for PR19 (a 437% increase).⁷

81. While this focus on facilitating investment is understandable, it may risk over-weighting short-term deliverability for the companies at the expense of long-term customer value. This is especially true given the broader set of risk mitigations built into PR24, which we detail below.

82.These adjustments mean that it is more likely that the companies will achieve or exceed the allowed WACC. The enhanced true-up and sharing mechanisms will reduce the expected variability of returns, especially the downside risk.

83. Ofwat explicitly considers the potential impact of the capital programme on beta in its WACC consideration. Ofwat correctly concludes:

“After considering new arguments and evidence from representations, we remained unconvinced that the characteristics of PR24 necessitated a departure from our long-standing approach of relying on econometric estimates from 'pure play' companies.”

84. In summary, Ofwat supports its conclusion by noting:

• average annual capex-to-RCV over the 2025-30 control period is 10.9%, and thus only slightly higher than the average over the past 15 years of 8.0%

• the link between higher capex intensity and higher undiversifiable (beta) risk is weak from a theoretical and empirical standpoint

• our final determinations provide enhanced risk protection to company performance on costs and outcomes compared to PR19, in ways we would expect to reduce beta risk

• it is rare in UK regulation to adjust econometric beta estimates in proportion to capex intensity

• adjusting econometric beta estimates carries an inherent risk of measurement error as well as a risk of double counting impacts

85. Figure 14 shows that PR24 expenditure is comparable with other benchmark levels. Ofwat concludes:

“... this [PR24] level of average capital intensity is by no means remarkable compared with controls from other sectors.”

86. We agree with this reasoning and further highlight that the consequences of a large investment programme should largely be diversifiable and therefore not impact the beta estimate.

87. We believe Ofwat’s conclusion on beta highlights a potential inconsistency. In terms of the cost of equity, the place where an uplift in risk would be expected to arise is in the beta. However, as Ofwat has concluded that it does not foresee an increase in beta from the PR24 capital programme, there does not seem to be a reasonable justification for increasing the allowed return.

88. There is a heightened degree of concern about the financial resilience of the sector and its ability to raise new capital. Ofwat rates 10 of 16 companies at elevated concern or higher for financial resilience.

89. We believe a major contributor has been the risky financial structures and high levels of gearing employed by the companies and their shareholders. The sector average gearing is close to 70% while the PR24 notional level is 55% (approximately £15 billion lower).

90. Further, the true level of gearing may be considerably higher when parent company debt and derivatives are included, for example Anglian’s parent company gearing is 85% (2024) while Southern has gearing at 95% and Yorkshire at 88% when derivatives are included (see Ofwat 2024).

91. Accordingly, we question:

• Could equity investors fund capex if debt is expensive or unavailable?

• Would notional efficient companies now use £15 billion of debt capacity to fund capex?

• If customers or financial markets have already funded £15 billion more capex?

92. Ofwat explains that it has adjusted the risk profile for its PR24 determination. It describes the process as “recalibrating” the risk and return package, saying:

“... we explain how our final determinations result in a material recalibration of the risk and return package for PR24 compared with the 2020-25 period, as a result of changes to our cost allowances, outcomes performance targets and application of cost sharing and risk protection measures.”

93. However, the outcome is a substantial reduction in the overall risk for shareholders. Ofwat estimates the quantum of the benefit arising to shareholders in expected return on equity to be in the order of an additional 3 to 5 percentage points compared to its draft decision. The benefit compared to PR19 will be greater. Ofwat said:

“Together these adjustments represent a material change to the risk and return balance that was set in our draft determinations. They reduce the overall downward skew that companies may have perceived to the expected return on equity by c.360 to 480 basis points had the draft determination been unchanged (114 to 228 basis points for cost allowances after cost sharing, 182 basis points for outcomes and 69 basis points for the allowed return).”

94. Ofwat provides a long catalogue of its changes. In summary these include:

• True-up and adjustment mechanisms

o Introduction of enhanced true-up mechanisms, including bringing forward the energy cost true-up.

o Application of outturn and RCV reconciliation adjustments, including the option to adjust via RCV rather than revenue.

o Expansion of uncertainty mechanisms coverage.

o Introduction of capped and separate mechanisms to address cost and outcome volatility.

• Cost sharing and incentive mechanisms

o General wholesale costs: capped at 60%

o Enhancement costs: lowered to 40% company share

o Specific investments, e.g., Industrial Emissions Directive: enhanced 25% company share

o Continuous water quality monitoring: 40% company share

o Business rates: reduced to 10% (from 25% at PR19)

o Introduction of aggregate sharing mechanisms for both outcomes and costs.

o Capping of PR19 cost sharing rate for 2024-25 to 60% on a retrospective basis.

• Cost allowances and expenditure increases

o Increase in base cost allowances to £60billion (7% above past spending).

o Possibility of additional base expenditure allowances.

o Recalibration of retail and wholesale cost allowances considering inflation.

o New delivery mechanism, e.g., for Thames and Southern Water, to allow extra expenditure claims for 2025-30.

o Extension of DPC and SIPR regimes covering 27 major projects.

o Formal gated allowances introduced for 13 large, complex investment projects (worth £2.3 billion).

o Increased protection from real price effects: ~55% of allowances indexed to benchmark rates, vs. 30% if only labour costs were indexed.

• Performance and outcomes

o Lowering of performance targets.

o Performance commitments aligned to sector median rather than upper quartile, as in PR19.

o Adjustments tied to quality and ambition assessments and ODIs.

• Financing, cashflow and RCV measures

o Increased RCV run-off rates to improve short-term cash flow.

o Option for companies to take outcome-based adjustments as RCV rather than revenue.

o Commitment to fund efficient costs associated with raising new equity via exchange listing.

95. From this catalogue we focus on 4 examples. Each example demonstrates a reduction in risk for the companies compared to PR19.

96. Ofwat has made performance targets easier to achieve by reducing them compared to PR19. Ofwat stated:

Our starting assumption at draft determinations was that companies would meet their PR19 PCLs and that we would only move away from them if there is compelling evidence to support a differentapproach.

97. In particular, companies and investors raised concerns about “…using PR19 performance commitment levels as a baseline for the 2025-30 period, given the sector's poor performance in the 2020-25 period to date”. We illustrate the impact of Ofwat’s decision on pollution incidents, internal sewer flooding and leakage in the following charts.

Figure 15: Number of pollution incidents per 10,000 km of the wastewater network: PR19 target and actual and PR24 targe

Figure 16: Number of internal sewer flooding incidents per 10,000 sewer connections: PR19 target and actualand PR24 target

Figure 17: Leakage: Percentage reduction in 3-year average from 2019-20 baseline: PR19 target and actualand PR24 target

98. Ofwat has introduced new in-period adjustment mechanisms to adjust allowances. They are material. Ofwat estimates that “… around 55% of total expenditure will be covered by true-ups related to external input price factors”. The complete list ofadjustments mechanisms are shown in the table below.

Table 8: PR24 in-period adjustment mechanisms

99. Ofwat has brought forward the true-up for energy prices:

“… our final determination pproach consists of an uplift to allowances using the DESNZ industrial energy price index, and subsequently a six-year RPE glidepath which eliminates the uplift by the end of the 2029-30 period.”

“In our view, this is a pragmatic approach as a 'cross-check' against market evidence and the historical lag between the DESNZ index and wholesale energy prices suggests that the DESNZ industrial price index could return to the long-run historical index value in a shorter time frame (e.g. three-years).”

100. Under the totex approach employed by Ofwat, it is necessary to specify the amount of RCV that will be returned to shareholders each year. Ofwat noted there is no consistent company view, saying:

“… there is no consistent company view as to how run-off rates should be set and no definitive view as to what is the 'correct' rate of runoff.”

101. Rather, the run-off rate is used:

“… to make proportionate adjustments to the timing of cash flows across price control periods for purposes of managing affor dability concerns and financeability constraints.”

102. Ofwat has increased run-off rates:

“Recognising the obligations that are on companies to maintain their asset bases, we have adopted a more cautious approach to our iterventions on RCV run-off for our final determinations. A consequence of this decision is an improvement to the cashflows of some companies compared with our draft determinations.”

“Primarily we have intervened where companies' proposed rates are outliers, where there is headroom versus historic cost depreciation and where there is headroom in our financeability assessment.”

103. The adopted run-off rates imply a remaining asset life in the order of 25 years. This seems low for long-lived water assets and suggests that owners are receiving their capital back at an accelerated rate. While improving financeability in the short term, this approach will cause problems in the future as the RCV is exhausted. Further evidence is that run-off rates generally exceed historic cost depreciation by a material margin.

Figure 18: Final determination RCV run-off rates versus historical cost depreciation

Source: Ofwat

105. Six companies have appealed Ofwat’s final determination including Anglian Water, Northumbrian Water, Thames Water, Southern Water, South East Water and Wessex Water.

106. These companies represent 6 of the 8 highest in size of regulatory gearing. All have regulatory gearing greater than 68%. Further, 5 of the 6 are categorised by Ofwat as elevated concern or higher for financial resilience, including the 3 companies categorised as action required. Figure 19 identifies the companies that have appealed with black arrows.

107. It will be very important for the CMA to abstract from the specific circumstances of each company and instead focus on the notional efficient company. Customers should not be unduly exposed to the costs and consequences of the risky financial strategies adopted by companies and their shareholders.

Figure 19: Gearing and Ofwat resilience rating (red box: action required; yellow box: elevated concern; blackarrow indicates appeal)

108. Ofwat estimates that average annual household bills, for water and wastewater, will increase by £157 between 2025 and 2030. Over the entire period, it projects an average real growth in bills of 36% for water and wastewater companies and 22% and water-only companies. These estimates are presented in Table 9 below.

Table 9 PR24 estimates of average household bills (2022-23 prices)

Source: Ofwat (2024). Note the simple average of 2024-25 water and wastewater bills is £445 not £440 – the discrepancy may be due to a small error. We note that the value for 2029-30 (£597) aligns with the simple average of the values shown.

109. These high-level estimates contain some important underlying features:

• all estimates are in real terms (“before inflation”);

• most of the increase is projected to occur in the first year of AMP8;

• the potential for further increases, e.g. subsequently approved projects;

• the potential further increases for Thames and Southern through company-specific delivery mechanisms.

110. To provide more context on the impact of Ofwat’s PR24 determination on household bills, we have constructed a continuous “spliced” series for average household bills by combining multiple sources of data from: Ofwat; Discover Water; and each company’s PR24 financial model, as published by Ofwat in December 2024.

111. Figure 20 shows the evolution of household bills since privatisation in nominalprices. All series are presented as given, except for the National InfrastructureCommission’s (NIC’s) series, which required a conversion from 21-22 prices intonominal prices

Figure 20 Average annual household bills since privatisation (water and wastewater)

Source: Ofwat (2019), Discover Water, Ofwat (2024) and NIC (2023). We also created a series using K-factor values published by Ofwat at each price review. The results of this were also consistent with the lines shown for Ofwat and NIC up until 2015. However, in PR14 Ofwat stopped publishing weighted average K-factor data, so we used simple average K-factor data from 2016, but the results are not as reliable, so we do not present them here.

112. There is a small discrepancy between the NIC and Ofwat datasets, but this does not change the general impression. In terms of accuracy, we take confidence from the observation that household bill estimates from Ofwat and Discover Water are consistent, as shown by the overlapping results for several years (16-17, 24-25, 25-26).

113. In line with Ofwat’s PR24 forecast, the Discover Water series shows a steep increase in household bills in the first year of AMP8. This increase reflects: Ofwat’s WACC; high inflation flowing into the RCV; and a large increase in expenditure allowances

114. Overall, Figure 20 shows that PR24 has resulted in a larger increase in bills than any other price control period.

115. For further context, Figure 21 presents household bills in 2022-23 prices.

Figure 21 Average annual household bills since privatisation (water and wastewater)

Source: Ofwat (2019), Discover Water, Ofwat (2024) and NIC (2023). Notes about these series: 1) we used CPI(H) to convert NIC’s and Ofwat’s historical series to 2022-23 prices; 2) Ofwat’s PR24’s estimates were calculated as a simple average of all water and wastewater companies’ estimates for each year, as provided in each company’s financial model already in 2022-23 prices; 3) To ensure continuity and comparability, we estimated the implied K factors from Discover Water’s series from 2017-18 to 2023-24 – after conversion from nominal to 2022-23 prices using CPI(H) – and used them to calculate the displayed values from 2018-19 to 2023-24. The K factors were calculated as the percentage annual growth of Discover Water’s series in real terms and were applied to the last value of Ofwat’s historical series, up to 2023-24.

116. AMP8 shows a sharp increase in real household bills compared with previous regulatory periods. Most of this increase is in the first year, with the average estimated growth at each year of the period being: 21.0%; 3.8%; 3.3%; 2.1%; and 2.5%.

117. Not only are bills expected to reach new all-time highs in nominal terms, but they are also projected to rise continually above inflation throughout AMP8. Ultimately, there fore, water bills are expected to have an increasingly larger weight in customers’ budgets during this period.

118. We have been engaged by the Consumer Council for Water (CCW) to provide expert services to review and analyse Ofwat’s Weighted Average Cost of Capital (WACC). We are asked to provide an independent assessment of the

appropriateness and potential impacts of Ofwat’s WACC methodology and assumptions.

119. We are to assess the extent to which Ofwat’s determination effectively balances the interests of customers whilst providing the necessary incentives for water companies and their investors. Our review is to consider Ofwat’s final PR24 WACC in the context of the overall risk and return framework.

120. Finally, we are asked for an opinion on whether the WACC is a balanced central estimate or is currently skewed e.g. standing to benefit shareholders at the expense of water customers.

121. This report has been prepared solely for the benefit of the client for the purpose described in the Introduction.

122. MCC Economics accepts no liability or duty of care to any person other than the client for the content of the report and disclaims all responsibility for the consequences of any person other than the client acting or refraining to act in reliance on the report or for any decisions made or not made which are based upon the report.

123. The information in the report is based upon publicly available information and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. In preparing the report, we have relied upon and assumed, without independent verification, the accuracy, completeness and reliability of information available from public sources. Nothing in this report constitutes a valuation or legal advice.

124. This report is based on information available to MCC Economics at the time of writing the report and does not consider any new information which becomes known to us after the date of the report. We accept no responsibility for updating the report.

125. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity.

126. No representation or warranty of any kind (whether express or implied) is given by MCC Economics to any person (except to the client under the relevant terms of our engagement) as to the accuracy or completeness of this report. responsibility and will not accept any liability in respect of this report to any partyother than the client.

127. The client may publish this report on its website to facilitate demonstration that a study into the matters reported has been performed. Publication of this report does not in any way or on any basis affect or add to or extend MCC Economics’ duties and responsibilities to the client or give rise to any duty or responsibility being accepted or assumed by or imposed on MCC Economics to any party except the client. To the fullest extent permitted by law, MCC Economics does not assume any responsibility and will not accept any liability in respect of this report to any party other than the client.

I was delighted that MCC's work was completed on time, and within budget, helping us deliver important changes and improvements, to the benefit of our stakeholders. MCC's report is published on the CCC website.

I am delighted to recommend MCC Economics. Specifically, I worked closely with PJ, who helped us with our Nuclear and CCUS projects. PJ helped us develop new policies and answer questions from our stakeholders. His support helped us deliver important changes and improvements, to the benefit of our stakeholders.

MCC Economics has helped us better understand the most important issues for our stakeholders, including: charges, shareholder returns, debt payments and inflation impacts.

I am delighted to recommend PJ and his team at MCC Economics. We've been working together on National Policy Statements to help meet net zero targets for 2030 and 2050. We initially appointed MCC Economics to support us on offshore wind consultation analysis and have recently reappointed MCC Economics to undertake a larger consultation analysis role across all sectors, including hydrogen, CCUS and networks. I can confirm that PJ and his team have shown excellent spreadsheet skills, alongside very good project management, planning and analysis skills, helping us deliver important changes, and continuous improvements, to the benefit of our stakeholders.

I am delighted to recommend PJ and his team from MCC Economics. They helped us with our price controls for Heathrow airport and for NATS (En Route) plc (the air traffic services provider). Specifically, the MCC team helped us deliver important changes and improvements to our financial models and supporting policy documents, to the benefit of our stakeholders.

I am delighted to confirm that I worked with PJ on a retail project in 2015. The project helped stakeholders understand electricity costs and charges. Specifically, the project helped us explain to stakeholders, internally and externally, why electricity charges differed across the regions (GB, NI & Ireland). PJ was a key member on the project team, which helped deliver changes and improvements in the understanding of energy retail.

.png)

Evidence-based analysis for transparent, defensible, and effective decision-making.

© All rights reserved – MCC Economics 2026.