Electricity North West Limited (ENWL), a regulated monopoly distributing electricity to 5 million customers across North West England, was acquired by Iberdrola in 2024 for €5 billion. MCC Economics’ publication examines the intricacies of this deal, including a significant 44% premium over ENWL’s Regulatory Asset Value (RAV). The analysis delves into ENWL’s financial inefficiencies, high cost of embedded debt, and regulatory challenges under Ofgem’s framework, juxtaposed with its strong equity performance and potential synergies with Iberdrola’s existing networks. This publication provides a comprehensive exploration of the value drivers, risks, and opportunities associated with the acquisition, offering valuable insights for investors and stakeholders in regulated utility markets.

This publication investigates the 2024 acquisition of Electricity North West Limited (ENWL) by Iberdrola, a transaction valued at €5 billion, including debt, and reflecting a substantial 44% premium over ENWL’s Regulatory Asset Value (RAV). ENWL serves as a regulated monopoly responsible for electricity distribution across North West England, supporting the UK’s decarbonisation goals. Key themes explored include ENWL’s financial challenges, regulatory constraints, and Iberdrola’s strategic motivations, including synergies with adjacent networks and growth potential in the transition to electrification. This case study offers critical insights into the valuation of utility assets, regulatory impacts, and the evolving energy landscape.

Recently, a large investor asked us to provide due diligence of a monopoly network company in the United Kingdom to support a M&A transaction.

Electricity North West Limited (ENWL) is a regulated monopoly responsible for electricity distribution across North West England. Serving 5 million customers, with approximately 60,000 km of electricity distribution networks, its operations power cities such as Manchester and Cumbria while advancing the UK’s decarbonisation goals.

Despite the large consumer base and revenue levels of about £580 million in the financial year 2024, ENWL’s acquisition by Iberdrola in 2024 motivated an investor debate over the company’s valuation.

The 2024 transaction was finalised at a valuation of €5 billion (£4.2 billion), including debt, with Iberdrola purchasing an 88% equity stake for €2.5 billion (£2.1 billion). This deal represented a 44% premium over ENWL’s Regulatory Asset Value (RAV) of £2.9 billion. This deal made the UK Iberdrola’s largest market by asset base.

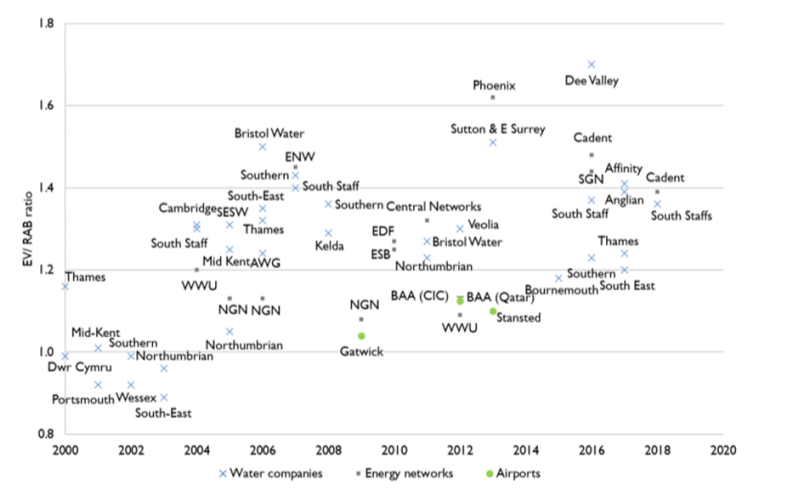

There is a consistent history of electricity network assets in the UK attracting significant premiums above the RAV. Figure 1 shows similar transactions over the past decade.

In this context, Iberdrola's investment does not seem out of range. However, there weresome unique characteristics of ENWL that were central valuation issues.

ENWL has faced persistent challenges with its cost of debt. The regulator, Ofgem highlighted these debt cost problems as far back as 2010. Regulatory reviews by Ofgem, when considering whether to fund ENWL's actual cost of debt, refer to inefficiencies and the risk to consumers. These higher costs have raised concerns about the company’s financeability under existing regulatory frameworks, as highlighted in its RIIO-2 business plan. Moody’s has further criticised the broader utility sector for its reliance on interest rate swaps, a strategy commonly referred to as “kicking the can down the road”. This approach temporarily alleviates financial pressures by deferring costs but leaves companies vulnerable to future economic fluctuations and rising interest rates. For ENWL, such practices have compounded its financing challenges, undermining its long-term financial resilience and heightening scrutiny from both regulators and investors. If these efficiencies carry to the new owner, then this would suggest a lower valuation. However, if the new owner is able to resolve these issues through its broader debt portfolio then there may not be much impact on value.

In its 2019 RIIO-2 business plan, ENWL said its business plan was “not financeable” under Ofgem’s regulatory framework. In particular, it raised concerns about its ability to attract sufficient investment to maintain and improve its infrastructure. This challenge stemmed from ENWL's comparatively high debt costs, which left it at a competitive disadvantage against peers operating with more efficient financial structures. ENWL argued that the regulatory allowance for financing costs did not adequately reflect its higher cost of debt, potentially jeopardising its capacity to meet future capital investment requirements and maintain service reliability. However, Ofgem rejected ENWL’s application for higher debt allowances during the RIIO-2 determinations. The Competition and Markets Authority (CMA) rejected similar requests from another utility company, WWU. These decisions underscored a regulatory principle that companies should bear responsibility for their own financial inefficiencies.

ENWL's Regulatory Financial Performance Report (RFPR) highlights its strong performance in critical areas of its Return on Regulatory Equity (RoRE), including totex efficiency, effective tax management, and strong reliability metrics under the Interruptions Incentive Scheme (IIS). Further, high inflation in recent years has improved ENWL’s debt results, materially dampening a previous weakness, given “an improved debt-funding position when inflation is high and a worse debt-funding position when inflation is low.”.

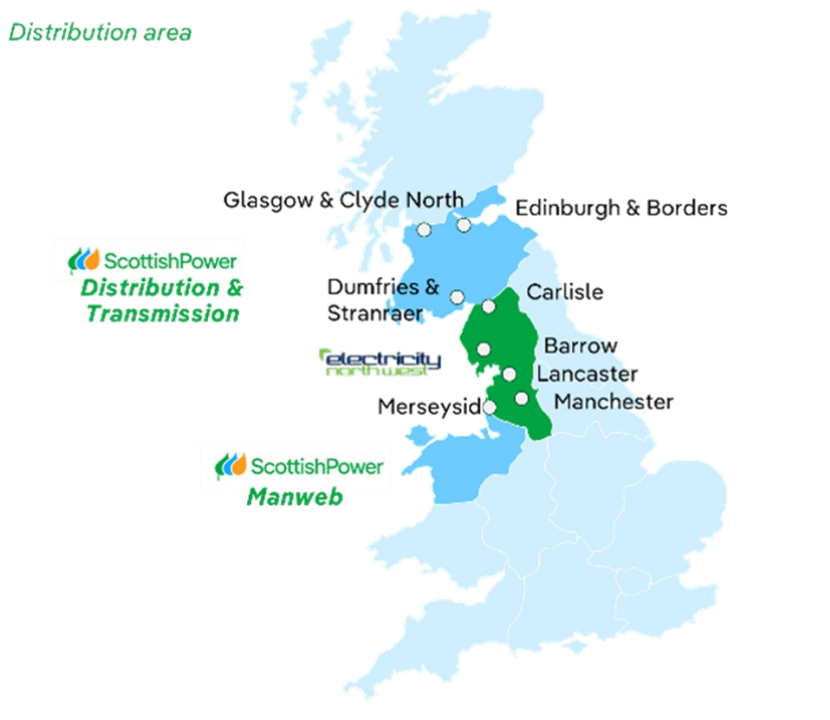

Geographically, ENWL is located between the two existing ScottishPower networks license areas owned by Iberdrola: central and southern Scotland and Merseyside and North Wales. See map below. This made Iberdrola a natural buyer with potential efficiency synergies from its adjacent franchises. It also opens joint electricity growth options in the transition from fossil fuels to electrification. Arguably ENWL is more valuable to Iberdrola than other buyers.

I was delighted that MCC's work was completed on time, and within budget, helping us deliver important changes and improvements, to the benefit of our stakeholders. MCC's report is published on the CCC website.

I am delighted to recommend MCC Economics. Specifically, I worked closely with PJ, who helped us with our Nuclear and CCUS projects. PJ helped us develop new policies and answer questions from our stakeholders. His support helped us deliver important changes and improvements, to the benefit of our stakeholders.

MCC Economics has helped us better understand the most important issues for our stakeholders, including: charges, shareholder returns, debt payments and inflation impacts.

I am delighted to recommend PJ and his team at MCC Economics. We've been working together on National Policy Statements to help meet net zero targets for 2030 and 2050. We initially appointed MCC Economics to support us on offshore wind consultation analysis and have recently reappointed MCC Economics to undertake a larger consultation analysis role across all sectors, including hydrogen, CCUS and networks. I can confirm that PJ and his team have shown excellent spreadsheet skills, alongside very good project management, planning and analysis skills, helping us deliver important changes, and continuous improvements, to the benefit of our stakeholders.

I am delighted to recommend PJ and his team from MCC Economics. They helped us with our price controls for Heathrow airport and for NATS (En Route) plc (the air traffic services provider). Specifically, the MCC team helped us deliver important changes and improvements to our financial models and supporting policy documents, to the benefit of our stakeholders.

I am delighted to confirm that I worked with PJ on a retail project in 2015. The project helped stakeholders understand electricity costs and charges. Specifically, the project helped us explain to stakeholders, internally and externally, why electricity charges differed across the regions (GB, NI & Ireland). PJ was a key member on the project team, which helped deliver changes and improvements in the understanding of energy retail.

.png)

Evidence-based analysis for transparent, defensible, and effective decision-making.

© All rights reserved – MCC Economics 2026.

.png)

%20(1).png)

.jpg)