This MCC insight distils what it takes to run power systems with very high renewables: better forecasting, faster connections, smarter planning, and a serious focus on flexibility. Explore the practical “playbook” for grid readiness, drawn from examples across the UK, Australia, and the Gulf.

The paper summarises critical enablers for high-renewable grids, spanning network planning, connections reform, and operational tools like forecasting and digital platforms. It highlights the importance of sequencing wires and flexibility investments (including storage and demand response) so renewables can connect and operate reliably. Using cross-market examples, it also discusses institutional arrangements (e.g., T&D structures), regulatory reforms that prioritise “shovel-ready” projects, and the role of collaborative scenario planning in accelerating build-out while maintaining security of supply.

• Scottish & Southern Electricity Networks

• ArchUp

• Reuters

• Australian Energy Market Operator

• UK – Demand Flexibility Service (DFS): In winter 2022/23, 1.6 million households and businesses participated, saving over 3.3 GWh of electricity during peak times. Incentives for consumers varied, with some third-party apps offering payments ranging from ≈£2.40–£2.70 per kWh saved during peak periods Energy UK Sunsave

Here are some options, including their potential rewards per kWh saved in the 2023/24 period:

• Loop Energy: This app paid around £2.50 per kWh saved (around 80% of what it received from National Grid ESO), redeemable through gift cards at the end of the 2023/24 scheme.

• Hugo Energy: Paying around £2.40 per kWh saved (at least 80% of what it received from National Grid ESO), the reward was redeemable via PayPal at the end of the 2023/24 scheme.

• Equiwatt: This app paid out the second best amount at around £2.70 per kWh saved (around 90% of what it received from National Grid ESO), redeemable through gift cards at the end of the 2023/24 scheme.

• Iv ie: Rather than paying out a set amount, this app allows you to earn entry points for various prize draws, ranging from weekly £25 Amazon vouchers to a £1,000 cash prize (the value of these equating to around 85% of what it received from National Grid ESO).

• uSwitch (Utrack): This app paid the top amount of £3 per kWh saved (100% of what it received from National Grid ESO), plus a bonus for first-time users, redeemable as a one-off payment at the end of the 2023/24 scheme.

• Abu Dhabi – DR Pilot Phase 2: launched May 2025, targets over 250 MW flexible demand capacity through the participation of 30+ leading industrial and commercial entities across the emirate, in collaboration with Energy Pool as the Demand Response Aggregator UAE Department of Energy

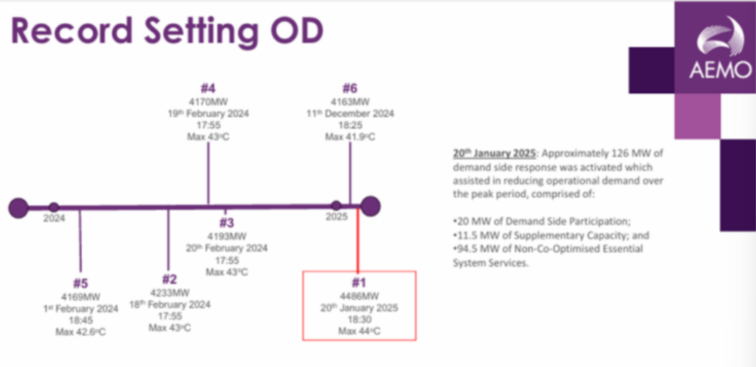

• Australia – Heatwave 20 Jan 2025: During WA’s 4,486 MW demand peak, AEMO activated 126 MW of demand-side response—20 MW DSP, 11.5 MW supplementary, and 94.5 MW ESS—helping avoid gas dispatch. Australian Energy Market Operator

These programmes flatten peaks, free transformer headroom and provide operatorswith rapid, software-based “virtual lines”.

New laws and regulations targeting the demand side include: 1) construction regulations to increase efficiency standards in buildings, 2) utility regulations to suppress vested interests, 3) dynamic tariffs and price signals, 4) mandatory and improved metering, 5) innovation funding, 6) demand aggregation rules, 7) open data, 8) Distributed Energy Resource Management System (DERMS), and 9) smart grid orchestration (including automated demand control)

• Blackhillock, Scotland – 200 MW/400 MWh Phase-1 live Mar 2025; will supply grid-stability services under ESO’s Pathfinder scheme. E&T Magazine

• Al Ajban PV – 1.5 GWac + 19 GWh BESS project to deliver 1 GW baseload clean power, reducing 2.4 MtCO₂/year; EPC awarded Jan 2025. Al Ajban | Saudi Gulf Projects | Sustainability Middle East News

• Waratah Super Battery – world’s largest grid-forming asset; provides a 700 MW “virtual shock absorber” to release 1.5 GW head-room across the Sydney-Newcastle corridor. Energy Corporation of New South Wales

Storage soaks up surplus solar, defers line upgrades, and supplies fast frequency response — key for 100% renewables ambitions.

• National Grid Electricity System Operator

• Australian Energy Market Operator

• UK – Connections Reform (TMO 4+): NESO paused new transmission applications from 29 Jan 2025 to address a 780+ GW queue and fast-track shovel-ready renewables NESO NESO

• UK – Offshore Transmission Network Review (OTNR) drives joint developer/ESO design of meshed offshore grids. Gov UK

• Abu Dhabi – TAQA restructuring: ADDC & AADC merged into TAQA Distribution Jan 2025, while TRANSCO became TAQA Transmission—creating clear, specialised T&D entities under one holding. TAQA

• Australia – NSW Transmission Planning Review 2025: A state-commissioned review now coordinates Transgrid, EnergyCo, AEMO and AEMO Services, with multiple public-consultation rounds, to reform how NSW plans and funds new lines under its Electricity Infrastructure Roadmap. Energy NSW

Source:

• AGSI

• AEMO

Abu Dhabi keeps functional unbundling: TAQA Transmission owns the 400/220 kV grid, while TAQA Distribution handles 11–33 kV supply. Being subsidiaries of the same holding eases data-sharing and investment alignment, avoiding the split-incentive issues seen in some liberalised markets.

The UK is synchronising by green lighting the EGL corridors alongside Scot Wind projects. Abu Dhabi approved the 19 GWh BESS and ICAD-4 substation before Al Ajban PV breaks ground. Australia, by contrast, built 10 GW renewables ahead of transmission and is now retrofitting (e.g., Waratah battery) while rushing VNI West—highlighting the cost of lagged sequencing.

UK connection reform and Ofgem’s RIIO-ED2 rewards for DSO flexibility show progress, but developers still face multi-year queues. Abu Dhabi’s mandatory DR participation rule is region leading. Australia’s NEM rule changes (Wholesale Demand Response & IESS) put flexible load and storage on equal market footing, yet local planning hurdles remain.

Joint scenario planning (NESO + DSOs DFES, AEMO IASR) and co-funded innovation (ESO Pathfinder, TAQA-Masdar AI projects) provide blueprints. Embedding social-licence metrics, as AEMO now does — builds public trust and accelerates builds.

90% looks feasible in the future, but the last 10% is currently difficult and expensive. Large-scale solar + multi-hour BESS (Al Ajban, 19 GWh) and emerging 250 MW pumped-hydro at Hatta cover intra-day balancing. Gas turbines equipped for green-hydrogen co-firing remain for seasonal backup.

1. Build wires & flexibility together: every £1 on HVDC or BESS can unlock ≥£2 in renewable capacity.

2. Demand-side programmes are scaling fast: 250 MW in Abu Dhabi, 1.6 M UK homes, providing “virtual” gigawatts.

3. Digital twins & AI forecasting: cut reserves and defer upgrades by double-digit percentages.

4. Storage is no longer optional: 400 MWh batteries (UK), 19 GWh hybrids (UAE) and grid-forming controls are now mainstream.

5. Regulation must keep pace: queue reform, social licence metrics and DSO incentives are the new competitive edge.

.png)

Explore our latest paper which examines Abu Dhabi’s solar approach—centralised utility-scale vs. distributed rooftop generation. Finds rooftop PV still uneconomical for heavily subsidised user groups but cost-effective for industry and commerce, suggesting subsidy reforms to unlock distributed solar for 2050 climate goals.

2022

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

Explore the forces behind ultra-low solar tariffs and why Dubai’s next PV + storage auction could be the world’s first step below 1¢/kWh.

225

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

-min.jpeg)

Discover how Ofwat’s Innovation Fund is shaping the future of water—what’s working, what’s blocking scale-up, and what regulators can do next.

2025

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

I was delighted that MCC's work was completed on time, and within budget, helping us deliver important changes and improvements, to the benefit of our stakeholders. MCC's report is published on the CCC website.

I am delighted to recommend MCC Economics. Specifically, I worked closely with PJ, who helped us with our Nuclear and CCUS projects. PJ helped us develop new policies and answer questions from our stakeholders. His support helped us deliver important changes and improvements, to the benefit of our stakeholders.

MCC Economics has helped us better understand the most important issues for our stakeholders, including: charges, shareholder returns, debt payments and inflation impacts.

I am delighted to recommend PJ and his team at MCC Economics. We've been working together on National Policy Statements to help meet net zero targets for 2030 and 2050. We initially appointed MCC Economics to support us on offshore wind consultation analysis and have recently reappointed MCC Economics to undertake a larger consultation analysis role across all sectors, including hydrogen, CCUS and networks. I can confirm that PJ and his team have shown excellent spreadsheet skills, alongside very good project management, planning and analysis skills, helping us deliver important changes, and continuous improvements, to the benefit of our stakeholders.

I am delighted to recommend PJ and his team from MCC Economics. They helped us with our price controls for Heathrow airport and for NATS (En Route) plc (the air traffic services provider). Specifically, the MCC team helped us deliver important changes and improvements to our financial models and supporting policy documents, to the benefit of our stakeholders.

I am delighted to confirm that I worked with PJ on a retail project in 2015. The project helped stakeholders understand electricity costs and charges. Specifically, the project helped us explain to stakeholders, internally and externally, why electricity charges differed across the regions (GB, NI & Ireland). PJ was a key member on the project team, which helped deliver changes and improvements in the understanding of energy retail.

.png)

Evidence-based analysis for transparent, defensible, and effective decision-making.

© All rights reserved – MCC Economics 2026.

.png)