%20(1).png)

This MCC piece sets the scene for a US–UK comparison series, highlighting why cross-country learning matters as both systems face ageing infrastructure, climate pressures, and rising expectations. Explore the governance and market differences, and what they mean for future reform choices.

The paper outlines key points of comparison between the US and UK water sectors, including ownership and governance structures, the role of regional planning and partnerships, and how innovation emerges in different institutional settings. It frames the value of looking at state-by-state US variation to identify adaptable approaches, and positions the series as a practical contribution to building more resilient, efficient, and sustainable water services in England and Wales.

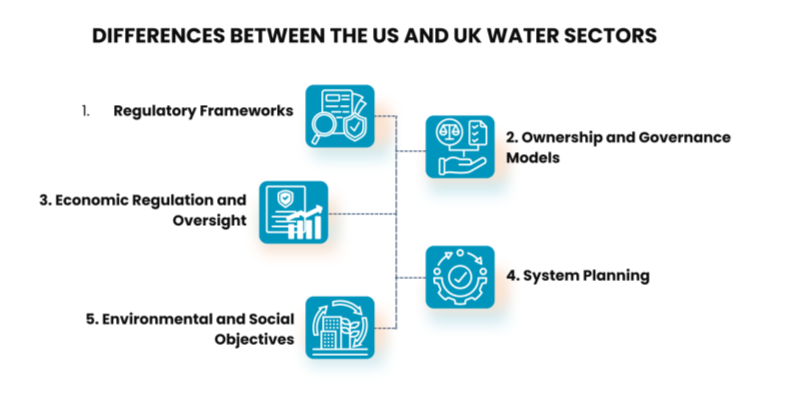

Water is a vital resource, and the structures that govern its provision and management reflect the diverse needs and contexts of different countries. The water sectors in the US and the UK each have unique regulatory and operational frameworks (ignoring the differences within the regions for now - i.e. England, Wales, Scotland and Northern Ireland each have their unique features). Yes, there are some similarities between the US and the UK (especially around challenges such as climate resilience, asset health and affordability) but in this article, we explore five key areas where their approaches diverge significantly.

The US and UK differ notably in their regulatory frameworks. In the US, economic regulation typically happens at the state level through state public utility commissions, while environmental protection is overseen federally by agencies like the Environmental Protection Agency (EPA) under laws like the Clean Water Act.

The Clean Water Act (CWA) establishes the basic structure for regulating discharges of pollutants into the waters of the United States and regulating quality standards for surface waters. The basis of the CWA was enacted in 1948 and was called the Federal Water Pollution Control Act, but the Act was significantly reorganized and expanded in 1972. "Clean Water Act" became the Act's common name with amendments in 1972.

Under the CWA, EPA has implemented pollution control programs such as setting wastewater standards for industry. EPA has also developed national water quality criteria recommendations for pollutants in surface waters.

In contrast, the UK uses a centralised economic regulatory approach, with Ofwat as the national economic regulator for England and Wales (Scotland is regulated by the Water Industry Commission while Northern Ireland is regulated by the Utility Regulator), complemented by environmental regulators – the Environment Agency (EA) in England and Natural Resources Wales in Wales. This structure is underpinned by a complex legislative framework that has developed over decades and is currently being called upon for review by some members of society, as reflected in the Independent Water Commission’s (IWC) recently published interim report.

The Environment Agency works to create better places for people and wildlife, and supports sustainable development.

EA is an executive non-departmental public body, sponsored by the Department for Environment, Food & Rural Affairs, supported by 1 public body.

The Commission recognises, in a system of regional monopoly companies, the necessity for an objective, industry-wide benchmarking framework to protect customers from misuse of monopoly power in relation to price and service levels and to set incentives for efficiency improvement. However, there are limits to how accurate such a benchmarking framework and econometric tools can be and the extent to which these can be relied upon. This is particularly true for the water industry in which water firms face very different challenges (for example, geography, hydrology, demography and history) and for which the public policy objectives have become more complex and demanding.

The Commission’s view is that a fundamental strengthening and rebalancing of the current approach to economic regulation is required. This should entail the development of a strong company-specific ‘supervisory’ function in the economic regulator alongside its econometric benchmarking function.

Ownership and governance structures show sharp contrasts between the two countries. In the US, a diverse mix of nearly 50,000 Community Water Systems (CWS) including municipal utilities, co-operatives, and private or investor-owned utilities provide services, while the UK has fewer than 30 regulated water companies, most of which operate as regional monopolies.

In the UK, privatisation in 1989 led to an exclusively private ownership model in England and Wales (while Scotland and Northern Ireland retained public control), with Dŵr Cymru (Welsh Water) being the only water company to operate under a not-for-profit holding company

The IWC report notes that ownership structures can shape performance and financial resilience, particularly through their approach to risk and return on investment.

The Commission’s current view is that, while there are important differences between listed and unlisted ownership models, the most important determinant of performance and resilience is the ‘business model’ of the

Research shows some interesting results on the economies of scale of the water sector(see for example Tynan & Kingdom, 2005 and Ferro et al., 2011).

In the UK, Ofwat sets price controls every five years through periodic reviews. These reviews determine customer bills by calculating allowances for costs such as operating expenses, capital investments, and the Weighted Average Cost of Capital (WACC).

The IWC report emphasises the importance of integrating both industry-wide benchmarking and company-specific supervision, to ensure balanced and effective regulation.

By contrast, the US lacks a national economic regulator (although federal agencies like the EPA influence investment indirectly through funding programs) which means that approaches to price setting and investment vary by state, creating a more decentralised landscape. Most of the economic regulation observed in the US is also company-specific, which allows for decisions that are more attuned to local needs.

The Commission recognises, in a system of regional monopoly companies, the necessity for an objective, industry-wide benchmarking framework to protect customers from misuse of monopoly power in relation to price and service levels and to set incentives for efficiency improvement. However, there are limits to how accurate such a benchmarking framework and econometric tools can be and the extent to which these can be relied upon. This is particularly true for the water industry in which water firms face very different challenges (for example, geography, hydrology, demography and history) and for which the public policy objectives have become more complex and demanding.

The Commission’s view is that a fundamental strengthening and rebalancing of the current approach to economic regulation is required. This should entail development of a strong company-specific ‘supervisory’ function in the economic regulator alongside its econometric benchmarking function.

System planning in the UK is another point of attention, as noted in the IWC’s recent report. The IWC report discusses the need for regional water system planning arrangements in England that would align investments and improvements across sectors at a river basin level.

In the US, system planning similarly occurs at the local and regional levels, often driven by municipal or regional authorities, given the absence of a national water grid. A decentralised approach would probably raise new issues of its own, although it seems that the IWC report believes the UK (strictly, England and Wales) can benefit from a more decentralised approach to system planning (without any explicit mention of the good/bad results from the US approach).

While only government can set the overarching strategic goals and priorities for water, ‘system planning’ – that is translating those goals into investment and improvement across sectors - must involve sub-government level actors, recognising the regional nature of our water systems and the diversity of demands we put on them.

At present, there is a complex patchwork of system planning and management arrangements in England and Wales that does not effectively bring together all the demands on regional water systems, the challenges that need to be met and all the actors that have an impact on water. The Commission has heard that local voices are lost in the system.

In parts of the country, a lack of joined-up water system planning has been a significant barrier to local development.

In north Sussex, the Commission has heard that local authorities are affected by ‘water neutrality,’ which requires local planning authorities to ensure that new development does not increase groundwater abstraction. This requirement was introduced by Natural England to prevent harm to habitats. As a result, local authorities have seen significant delays to delivering essential infrastructure such as new schools and housing. There have been decades of under-delivery in Southern Water’s WRMPs, which have contributed to these water resource issues. The EA and Southern Water have had disagreements about whether the company’s abstraction licence should be revoked in the affected area, with Southern Water saying that keeping the licence in their WRMP is in line with legislation.

This demonstrates the complexity of water system planning at a local level, with regulators, local governments, and water companies all facing different, often competing, incentives. The absence of a clear decision-maker and robust accountability mechanisms for delivery, combined with poor communication between actors in the system and a failure to account for broader requirements and costs, has undermined delivery of local priorities. The burden of water neutrality has fallen mainly on local planning authorities and the development sector despite most of the levers to address underlying issues being outside of their control. It is clear that a lack of coherent systems planning can undermine local growth and development, damage the environment, and waste valuable regulator and local authority time and resources.

Both countries have strong environmental protection frameworks, though recent performance and enforcement challenges - particularly in the UK (especially England and Wales)- have sparked public and political concern. England and Wales has national targets for water quality and ecosystem health, such as the objective for 75% of surface water bodies in England and 94% in Wales to achieve Good Ecological Status by 2027.

The lack of strategic direction for the water system has also been clearly highlighted by the lack of progress on the Good Ecological Status (GES) objectives set by the Water Framework Directive (WFD) Regulations regarding water quality. The ambition is for 75% and 94% of surface water bodies in England and in Wales respectively to achieve ‘GES’ by 2027. However, at the last classification (2019 in England and 2021 in Wales), only 16% of water bodies assessed in England and 40% in Wales reached this standard or better. There is no published plan for this past 2027 and, given current progress, the 2027 objective will be missed. The Commission has heard that implementation of the WFD regime has suffered from a lack of strategic prioritisation of objectives leading to short-term prioritisation of cost-savings over environmental outcomes, poor integration of all sectors that impact the water environment, and a lack of interim milestones to guide progress towards the long-term target.

13.—(1) The environmental objectives referred to in regulation 12 are, subject to regulations 14 to 19, the following objectives for the relevant type of water body or area.

(2) For surface water bodies, the objectives are to—

(a) prevent deterioration of the status of each body of surface water;

(b) protect, enhance and restore each body of surface water (other than an artificial or heavily modified water body) with the aim of achieving good ecological status and (subject to paragraph (3)) good surface water chemical status, if not already achieved, by 22nd December 2021;

(c) protect and enhance each artificial or heavily modified water body with the aim of achieving good ecological potential and (subject to paragraph (3)) good surface water chemical status, if not already achieved, by 22nd December 2021;

(d) aim progressively to reduce pollution from priority substances and aim to cease or phase out emissions, discharges and losses of priority hazardous substances.

(3) The objectives in paragraph (2)(b) and (c) are to be read as though they referred to achieving good surface water chemical status—

(a) in relation to substances 2, 5, 15, 20, 22, 23 and 28 in the table of priority substances, by 22nd December 2021;

(b) in relation to substances 34 to 45 in the table of priority substances, by 22nd December 2027.

In the US, water quality standards are set at the federal level by the EPA, under frameworks such as the Clean Water Act. These standards cover a range

Both countries face infrastructure and investment challenges. In the US, aging infrastructure and limited access to capital for small systems are key issues. The UK has similar concerns, with the IWC report noting a need for a forward-looking asset health and resilience framework (in England and Wales). This would ensure that infrastructure renewal is based on clear assessments of condition and future pressures, such as climate change and population growth.

In the US, water quality standards are set at the federal level by the EPA, under frameworks such as the Clean Water Act. These standards cover a range of 9 of 12 environmental protections, including surface water quality, storm water management, and drinking water safety. States are responsible for implementing and enforcing these standards through permitting and oversight of water systems. While there is flexibility for states to tailor implementation, there is a strong emphasis on maintaining compliance with national environmental goals, ensuring that local practices align with overarching federal requirements for safe, clean water.

In the Commission’s view, the current overarching legal requirements, regulatory activity and financial incentives do not appear to have led to a sufficient, forward-looking understanding of the health of water industry infrastructure. Assets have not been – and have not been required to be – fully mapped. Ofwat’s methodology for funding is backward looking, based on lagging maintenance expenditure and indicators of health. And there are no consistent standards against which companies can assess the health of their assets.

The Commission’s current view is that there is a strong case for a single, comprehensive infrastructure resilience framework across all water companies in England and Wales, which includes (i) establishment of resilience standards, (ii) a requirement for water companies to gather and report data on their assets and (iii) a more supervisory role for the regulator to enable a better understanding of an individual company’s assets and more tailored regulation, including in the setting of allowances and performance targets.

Resilience standards should ensure all companies make forward-looking, long-term assessments of asset health and of their ability to recover from disruption to critical infrastructure. They should be outcome focused, rather than focused solely on how long an asset should last, so where assets have back-up or redundancy, that can be factored into the assessment. The framework could also provide guidance for how companies could meet resilience standards without stipulating a particular course of action, to allow companies to identify the most efficient approach.

Despite structural differences, important parallels exist:

• Both water sectors face challenges with affordability.

• Both need to invest in ageing infrastructure.

• Both must adapt to climate change.

• Both recognise the importance of strengthening cross-sector collaboration.

• Both emphasise including local and regional voices in water planning.

These differences and similarities can provide important insights and opportunities for the UK to learn from the US experience. The size and diversity of the US, with its many states each adopting different approaches to water regulation, ownership and operation, create a diverse set of case studies that the UK can draw from. From local system innovation and regional planning partnerships to different models of utility ownership and governance, these examples can offer insights and potential strategies for addressing the challenges identified in the water sector of England and Wales

By examining how different states and regions in the US have tackled similar issues, the UK may find adaptable solutions that can be applied to its own regulatory, operational, and environmental landscape. The water sectors in both countries are evolving to meet the demands of the future. As they do, continued dialogue and sharing of experiences can help build more resilient, efficient, and sustainable water services for all

Over the coming weeks, we are publishing a series of posts here on LinkedIn where wewill explore in greater depth the differences and similarities between the US and UKwater sectors. We will look closely at possible lessons that the UK can take from the USexperience to address some of its most pressing water sector challenges, using the IWCreport as a starting point for assessing the most important issues. By examining theseinsights, we hope to contribute to a more resilient, effective, and customer-focusedwater sector for the future. Stay tuned for the next articles in this series.

Master financial modeling with our guide - simplified insights for effective planning, structure, and future adaptability

2021

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

Explore how distributed solar generation can transform Abu Dhabi’s energy landscape. Our report reveals the economic and environmental benefits of solar adoption, and accelerated progress toward the UAE's net-zero targets.

2021

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

.png)

Drawing from international examples, the submission offers insights on balancing retailer flexibility with consumer protection and proposes alternative approaches for effective implementation.

2024

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

Unordered list

Bold text

Emphasis

Superscript

Subscript

I was delighted that MCC's work was completed on time, and within budget, helping us deliver important changes and improvements, to the benefit of our stakeholders. MCC's report is published on the CCC website.

I am delighted to recommend MCC Economics. Specifically, I worked closely with PJ, who helped us with our Nuclear and CCUS projects. PJ helped us develop new policies and answer questions from our stakeholders. His support helped us deliver important changes and improvements, to the benefit of our stakeholders.

MCC Economics has helped us better understand the most important issues for our stakeholders, including: charges, shareholder returns, debt payments and inflation impacts.

I am delighted to recommend PJ and his team at MCC Economics. We've been working together on National Policy Statements to help meet net zero targets for 2030 and 2050. We initially appointed MCC Economics to support us on offshore wind consultation analysis and have recently reappointed MCC Economics to undertake a larger consultation analysis role across all sectors, including hydrogen, CCUS and networks. I can confirm that PJ and his team have shown excellent spreadsheet skills, alongside very good project management, planning and analysis skills, helping us deliver important changes, and continuous improvements, to the benefit of our stakeholders.

I am delighted to recommend PJ and his team from MCC Economics. They helped us with our price controls for Heathrow airport and for NATS (En Route) plc (the air traffic services provider). Specifically, the MCC team helped us deliver important changes and improvements to our financial models and supporting policy documents, to the benefit of our stakeholders.

I am delighted to confirm that I worked with PJ on a retail project in 2015. The project helped stakeholders understand electricity costs and charges. Specifically, the project helped us explain to stakeholders, internally and externally, why electricity charges differed across the regions (GB, NI & Ireland). PJ was a key member on the project team, which helped deliver changes and improvements in the understanding of energy retail.

.png)

Evidence-based analysis for transparent, defensible, and effective decision-making.

© All rights reserved – MCC Economics 2026.

.png)