Dive into MCC Economics' in-depth review of the Phoenix Energy acquisition, focusing on its valuation, regulatory framework, and the broader energy market dynamics. With exclusive gas distribution rights across Greater Belfast, Phoenix Energy faces both challenges and opportunities in the shift towards renewable energy. This case study examines the company’s performance within Northern Ireland’s unique regulatory environment, the implications of stranded assets, and the potential pace of electrification. The report also considers the strategic value of this acquisition for CK Infrastructure Holdings and its alignment with global trends in sustainable energy.

This publication provides a comprehensive analysis of the 2024 acquisition of Phoenix Energy by CK Infrastructure Holdings, valued at approximately £760 million. Phoenix Energy operates as the sole gas distributor in Greater Belfast and has rebranded to reflect its renewable energy aspirations. The report evaluates the deal’s valuation metrics, highlighting a rare alignment with its regulatory asset base, and discusses the risks posed by stranded assets and the potential acceleration of electrification. It further explores the implications of Northern Ireland’s regulatory framework, which supports renewable gas solutions while promoting continued gas network connections. This case study serves as a key reference for stakeholders in mergers, acquisitions, and regulatory policy within the energy sector.

Recently, a large investor asked us to provide due diligence of a monopoly network company in the UK Ireland to support an M&A transaction.

Phoenix Energy, established in 1996, operates with exclusive gas distribution rights across the Greater Belfast area. It was rebranded in 2023, from Phoenix Natural Gas to Phoenix Energy, to reflect renewable energy aspirations (biomethane and hydrogen). This transition aligns with Northern Ireland's energy strategy, which notes a phasing out of natural gas in favour of green alternatives and with the gas companies’ phase-in of green alternatives.

Phoenix Energy’s infrastructure is connected to 250,000 properties, and the projected revenue for 2024 stands at approximately £85 million, as per the Utility Regulator’s (UR) “Pi Model.” Its estimated Total Regulatory Value (TRV), a measure commonly referred to as the Regulatory Asset Base (RAB), Regulatory Asset Value (RAV), or Regulated Capital Value (RCV) in similar circumstances, in 2024 is estimated by UR at around £760 million.

In 2024 CK Infrastructure Holdings (CKI) purchased Phoenix for ~£760 million, which is very close to Phoenix’s TRV. It represents a multiple of just 1.0x and a premium to TRV of 0% - as close as we’ve seen to a discount to a regulated asset value. Does that make it a bargain? Let's take a closer look.

Investors, including our client, were interested in the following valuation issues:

1. Will green goals cause stranded assets? Gas, while a lower-carbon option compared to oil and coal, still emits carbon dioxide during combustion. This has led to increasing scrutiny and long-term risks of “stranded assets” as energy markets pivot to electricity and renewables like hydrogen and biomethane. Phoenix, on the other hand, states its infrastructure is adaptable for renewable gas solutions.

2. Should we be worried about UR’s regulatory framework? Phoenix Energy operates under a distinctive financial and operational model, overseen by the UR, which is very different from GB & European comparators. The financial model is unique and old. Phoenix has a unique approach to profiling cash flows, for example, which sets it apart from almost every other gas distribution company. Tax costs are under-funded and there are problems with the WACC allowance calculation, on first glance.

3. Why did Phoenix raise a price control appeal? In 2014, Phoenix successfully appealed a regulatory price control, arguing that certain incentive mechanisms should be included within the asset base to earn regulated returns, effectively increasing its TRV.

4. How quickly will electricity replace gas? The International Energy Agency (IEA) notes in its 2023 Energy Outlook report that:

“Energy transitions rely on electrification and technologies like wind, solar PV, and batteries, and push electricity security and diversified supply for clean technologies and critical minerals up the policy agenda.”

One useful backdrop to these questions is the analysis we conducted at the UKRN in 2016, comparing Phoenix (PNGL at the time) with Firmus Energy (FE) and other GB gas network companies as shown below:

Most significantly, the value of existing gas networks is influenced by your judgement on the expected pace of electrification and the potential viability of renewable gas or hydrogen.

In Australia, on 30 September 2024, AusNet submitted a variation proposal to the AER in respect of its gas distribution network in Victoria. AusNet stated that decisions by the Victorian Government including a ban on new gas connections meant that the pace of electrification would accelerate. Further, AusNet stated:

“The renewable gas path is now increasingly unlikely for Victorian Households, with hydrogen and renewable gases a possible option only for the hard to abate industrial sector.”

- Source: AusNet 30 September 2024, Access Arrangement Information, Gas Access Arrangement 2024-28, Variation proposal.

AusNet is seeking higher levels of accelerated depreciation to return its capital base to its owner.

However, the situation in Northern Ireland is quite different. The Utility Regulator recently stated:

In December 2021, the Department for the Economy (DfE) published its new Energy Strategy, “A path to net zero energy.” The strategy highlights the intention to utilise our modern gas infrastructure and the potential to generate and import zero carbon gases as a means of decarbonisation. While work is already underway to facilitate the injection of biomethane into the network, the route to fully decarbonised gas is uncertain and a further consultation has been identified within the Northern Ireland Energy Strategy on decarbonising heat.

In the meantime, as natural gas has lower emissions than oil, the Northern Ireland Energy Strategy continues to support connections to the gas network, while recognising that it is not economic or viable to extend the network to all homes.

While 308,000 properties have connected to the gas network at the end of 2021, there will still be around 247,000 properties close to a gas main which will not have connected (sic). The GD23 price control continues to support connections to the gas network by providing for a free connection when the connection is made, with the cost of the connection paid for by all consumers over a period of time

As you can see, gas connections are banned by the Victorian government in Australia, whereas in Northern Ireland, we give them away for free, and there's plenty of growth potential.

This Phoenix Energy transaction is a useful case study for other companies/investors in the gas sector who are involved in any merger, acquisition, divestment or regulation activity.

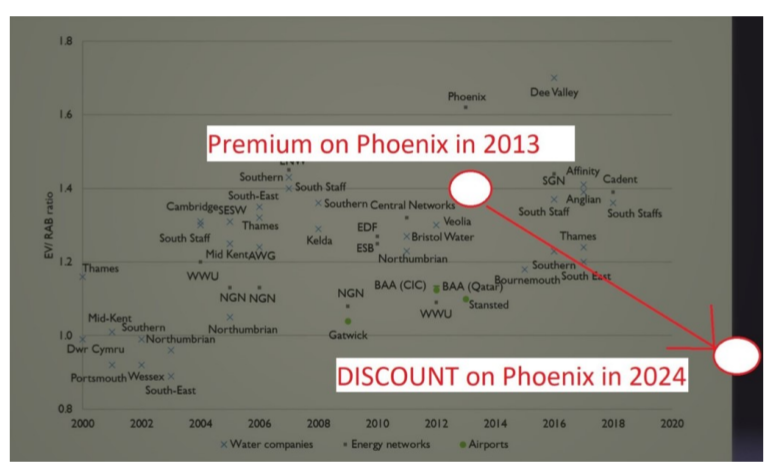

For context, in 2013, private equity group Terra Firma sold Phoenix to Hastings (on behalf of the Royal Bank of Scotland pension plan and Utilities Trust of Australia) for about £700m. That represented a large premium to TRV of nearly 40%.

The chart below puts this into perspective relative to similar utility assets over time, which normally trade at a premium to their asset value.

Accordingly, you may believe that investors are pessimistic on gas distribution and/or Northern Ireland investments going forward. On the other hand, maybe the new investor got a bargain. CKI said “We are very happy to acquire another quality asset characterised by stable returns,” CKI’s Victor Li Tzar-kuoi. (LinkedIn)

Interestingly, within months of the Phoenix transaction, another investor sought our guidance on acquiring “inflation-proof assets with stable income and stable regulation.” When asked about pricing, the other investor indicated willingness to pay up to a 30% premium on asset value for gas network assets.

Overall we’re surprised other investors and M&A teams did not join the race - few monopoly network assets can be bought cheaper (if you know of any – let us know).

Probably a great-value-buy for CK Infrastructure Holdings Limited, but some risks from electrification.

Interesting exit for Hastings Funds Management / RBS NatWest Group NatWest International / UToA.

I was delighted that MCC's work was completed on time, and within budget, helping us deliver important changes and improvements, to the benefit of our stakeholders. MCC's report is published on the CCC website.

I am delighted to recommend MCC Economics. Specifically, I worked closely with PJ, who helped us with our Nuclear and CCUS projects. PJ helped us develop new policies and answer questions from our stakeholders. His support helped us deliver important changes and improvements, to the benefit of our stakeholders.

MCC Economics has helped us better understand the most important issues for our stakeholders, including: charges, shareholder returns, debt payments and inflation impacts.

I am delighted to recommend PJ and his team at MCC Economics. We've been working together on National Policy Statements to help meet net zero targets for 2030 and 2050. We initially appointed MCC Economics to support us on offshore wind consultation analysis and have recently reappointed MCC Economics to undertake a larger consultation analysis role across all sectors, including hydrogen, CCUS and networks. I can confirm that PJ and his team have shown excellent spreadsheet skills, alongside very good project management, planning and analysis skills, helping us deliver important changes, and continuous improvements, to the benefit of our stakeholders.

I am delighted to recommend PJ and his team from MCC Economics. They helped us with our price controls for Heathrow airport and for NATS (En Route) plc (the air traffic services provider). Specifically, the MCC team helped us deliver important changes and improvements to our financial models and supporting policy documents, to the benefit of our stakeholders.

I am delighted to confirm that I worked with PJ on a retail project in 2015. The project helped stakeholders understand electricity costs and charges. Specifically, the project helped us explain to stakeholders, internally and externally, why electricity charges differed across the regions (GB, NI & Ireland). PJ was a key member on the project team, which helped deliver changes and improvements in the understanding of energy retail.

.png)

Evidence-based analysis for transparent, defensible, and effective decision-making.

© All rights reserved – MCC Economics 2026.

.png)

%20(1).png)

.jpg)