Can the UAE push solar tariffs below 1¢/kWh? This commentary examines the economics behind record-setting PV prices, using Al Dhafra as the benchmark and the upcoming MBR Solar Park Phase VII as the next test. We highlight the market conditions, procurement design, and technology shifts that could make another price breakthrough plausible.

Building on the UAE’s 1.32¢/kWh Al Dhafra outcome, the paper assesses whether forthcoming utility-scale PV tenders, especially Dubai’s MBR Solar Park Phase VII could break the sub-1¢/kWh barrier by 2027. It summarises the benchmark project’s key characteristics, reviews the sustained downward trend in solar LCOE across GCC mega-projects, and discusses Phase VII’s hybrid PV-plus-storage structure (including large-scale BESS integration). The note outlines drivers that could compress costs further—financing, supply chains, and module technology, and provides a directional price outlook.

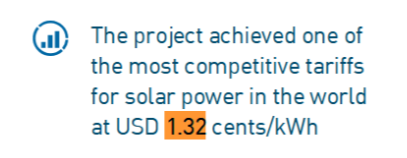

In 2023, the UAE’s Al Dhafra Solar PV project achieved the world’s lowest recorded solar tariff at just 1.32 ¢/kWh (≈0.05 AED/kWh). As bidding opens soon for Phase VII of the Mohammed bin Rashid Al Maktoum (MBR) Solar Park, a bold question emerges:

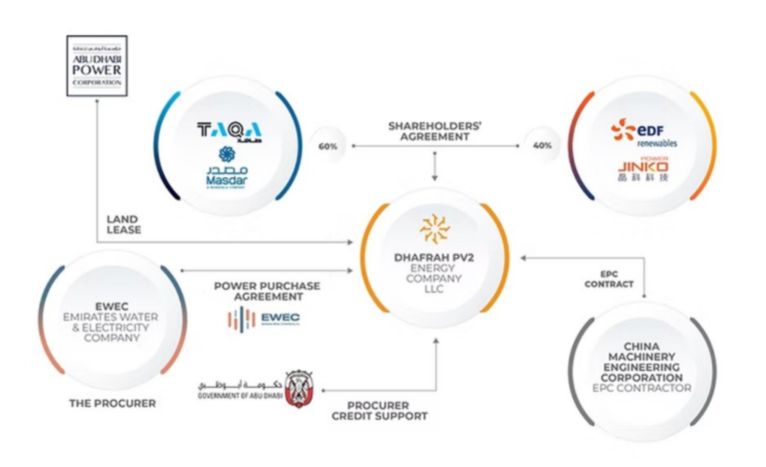

The 2 GW Al Dhafra project was developed by a consortium including TAQA, Masdar, EDF Renewables, and JinkoPower, and it now powers over 200,000 homes while displacing 2.4 million tonnes of CO2 annually.

• Tariff: 1.32 ¢/kWh

Location: 35 km south of Abu Dhabi city

The record-breaking project, located approximately 35 kilometers from Abu Dhabi city, has a capacity of 2 gigawatts (GW) and supplies power to the plant’s off-taker, Emirates Water and Electricity Company (EWEC). Upon completion in June 2023, Al Dhafra was the world’s largest single-site solar plant, using almost 4 million bifacial solar panels to generate enough electricity for approximately 200,000 homes across the UAE, displacing 2.4 million tonnes of carbon emissions annually.

The plant deploys the latest in crystalline, bifacial solar technology, which delivers electricity to the highest efficiency enabling the plant to provide more power by using both the front and back of the panels.

• Technology: Bi-facial solar panels + single axis tracking Dhafrah Energy

• Backing: International finance from 7 banks NS Energy Business

This graph shows Levelized Cost of Electricity (LCOE) in AED/kWh for major centralised solar projects across the GCC. We can notice a consistent downward trajectory

In less than a decade, solar costs in the UAE have plummeted from 0.21 AED/kWh (MBR Phase 2) to 0.05 AED/kWh (Al Dhafra) – a 76% reduction.

DEWA’s Phase VII project aims to add 1,600–2,000 MW of solar PV capacity plus 1 GW of battery storage. Commissioning is targeted for August 2027. Solar Quarter

The new phase will add 1,600 MWac to 2,000 MWac of solar photovoltaic (PV) capacity and integrate 1GW of battery storage, providing six hours of energy storage to ensure dispatchable clean power.

• First-time integration of large-scale 6-hour BESS (Battery Energy Storage System)

• Hybrid auction design: PV + storage PPA

• Supported by falling module costs and stronger local supply chains

Source: PV Magazine | ConstructionWeek

• UAE's solar resource: Global top-tier irradiance at >2,000 kWh/m2/yr

The Middle East and North Africa (MENA), a major oil and gas region, is now experiencing a growing focus on renewable energy, particularly solar PV. Amidst a surge in industrialization, persistent population growth, and economic development, coupled with concerns over climate change and environmental sustainability, solar power has emerged as a key component of the energy strategies of MENA nations. The region boasts one of the highest levels of solar energy potential globally, with an average annual solar irradiance exceeding 2,000 kWh per square metre per year, with standout countries including Saudi Arabia, UAE, Morocco, and Egypt.

• Policy support: Clean Energy Strategy 2050 and Net Zero by 2050

• Financing advantage: Sovereign-grade credit and long-term PPAs

• Tech innovation: Tandem and bifacial modules, AI-driven O&M

• Procurement scale: Centralised planning by DEWA, EWEC, Masdar

Most Likely Scenarios for Beating the Record:

• Bifacial + tracking combo + local module production cuts BoS costs

• Low-cost financing from UAE banks, SWFs, or export credit agencies

• Competition pressure from global EPC giants entering UAE tenders

• Excess polysilicon capacity drives module prices even lower in 2025–26

I was delighted that MCC's work was completed on time, and within budget, helping us deliver important changes and improvements, to the benefit of our stakeholders. MCC's report is published on the CCC website.

I am delighted to recommend MCC Economics. Specifically, I worked closely with PJ, who helped us with our Nuclear and CCUS projects. PJ helped us develop new policies and answer questions from our stakeholders. His support helped us deliver important changes and improvements, to the benefit of our stakeholders.

MCC Economics has helped us better understand the most important issues for our stakeholders, including: charges, shareholder returns, debt payments and inflation impacts.

I am delighted to recommend PJ and his team at MCC Economics. We've been working together on National Policy Statements to help meet net zero targets for 2030 and 2050. We initially appointed MCC Economics to support us on offshore wind consultation analysis and have recently reappointed MCC Economics to undertake a larger consultation analysis role across all sectors, including hydrogen, CCUS and networks. I can confirm that PJ and his team have shown excellent spreadsheet skills, alongside very good project management, planning and analysis skills, helping us deliver important changes, and continuous improvements, to the benefit of our stakeholders.

I am delighted to recommend PJ and his team from MCC Economics. They helped us with our price controls for Heathrow airport and for NATS (En Route) plc (the air traffic services provider). Specifically, the MCC team helped us deliver important changes and improvements to our financial models and supporting policy documents, to the benefit of our stakeholders.

I am delighted to confirm that I worked with PJ on a retail project in 2015. The project helped stakeholders understand electricity costs and charges. Specifically, the project helped us explain to stakeholders, internally and externally, why electricity charges differed across the regions (GB, NI & Ireland). PJ was a key member on the project team, which helped deliver changes and improvements in the understanding of energy retail.

.png)

Evidence-based analysis for transparent, defensible, and effective decision-making.

© All rights reserved – MCC Economics 2026.

.jpg)